微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

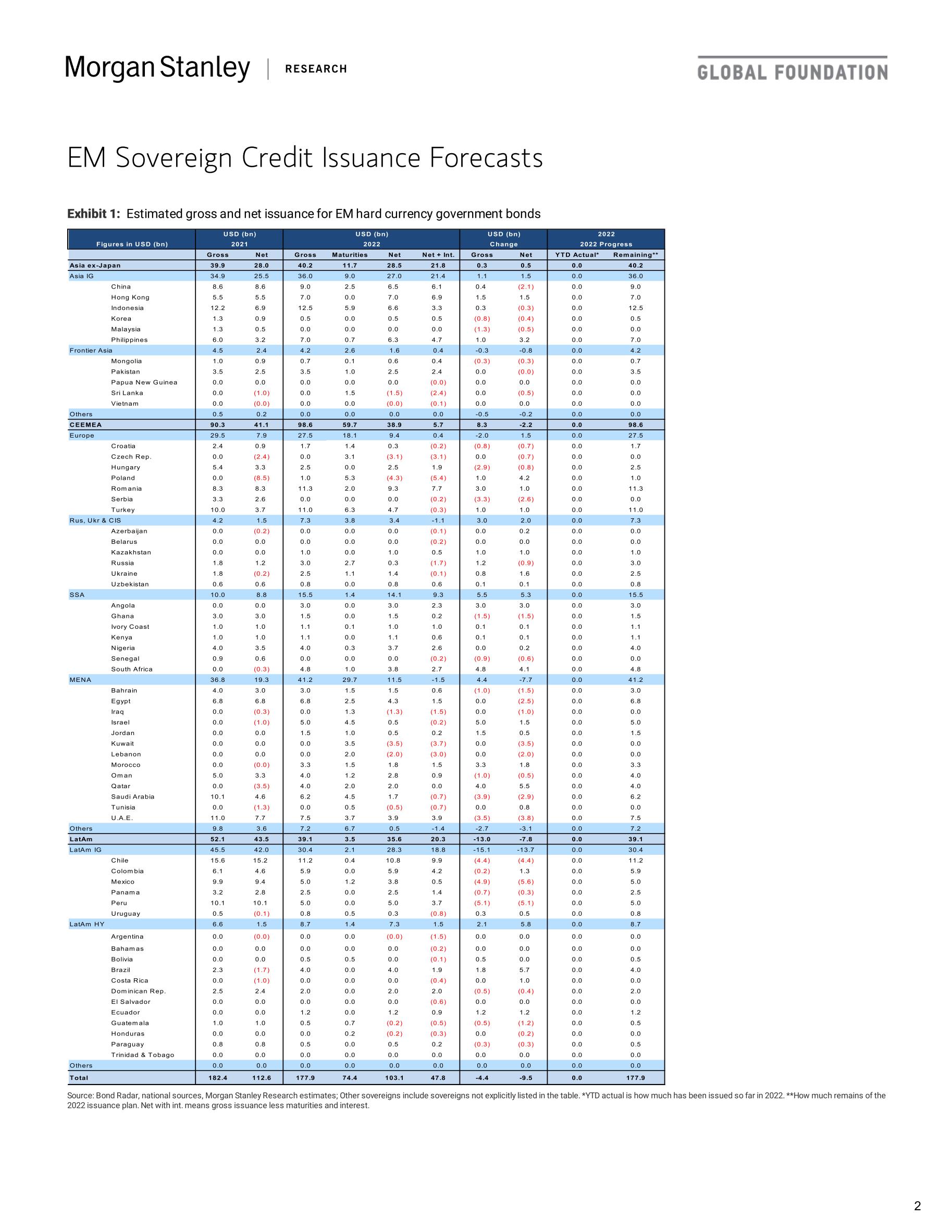

2022 sovereign gross issuance to fall to US$178bn: We estimate sovereign gross hard currency bond issuance to fall to US$178bn in 2022 from US$182bn in 2021 for the countries/regions covered in Exhibit 1, a drop of US$4bn. For these sovereigns, it would mean net issuance falls by US$10bn to stand at US$103bn, the lowest since 2015, given that maturities increase further. Once including interest as well, net payments stand at US$48bn.

The fall in gross issuance in 2022 versus 2021 comes mainly from LatAm IG, with MENA only down in net terms: In LatAm, most IG sovereigns should see less issuance despite remaining high versus history, with Chile, Mexico and Peru all expected to issue around US$5bn less versus 2021. In MENA, while gross issuance does increase by US$4bn, this is largely due to the high maturities, with net supply instead down by US$8bn, which is more in line with higher oil prices.

At a sovereign level, only four issuers are expected to issue more than US$10bn, namely Indonesia, Romania, Turkey and Chile.

Despite upward adjustments, budget oil price assumptions remain cautious: Higher oil prices were a key driver behind lower-than-expected issuance in 2021.

For 2022, the average price assumption of just US$57/bbl remains far below our commodity strategists' oil price expectations for 2022, suggesting that room for revenue outperformance remains. In turn, this should result in net issuance for EM oil exporters continuing to fall into 2022.

2022 to see more HY issuance, still high long duration issuance and even more ESG issuance: We expect HY issuance to be up by US$5bn to US$63bn while IG issuance falls by US$7bn to US$115bn for a HY share of 35% versus 33% in 2021.

2021 saw US$67bn of long-end bonds (+15y) for a 37% share, with 2022 likely to see just as high a number. EM sovereign ESG-labelled issuance more than tripled in 2021 to stand at US$33bn, or 18% of the total issuance. The largest growth came from social and sustainable bonds, with green bonds up slightly. This trend is set to continue, with new ESG issuers likely in 2022.

Lower local issuance versus 2021: EM ex China should see lower bond issuance on aggregate given that most economies continue to consolidate fiscal deficits post-pandemic, although levels remain wide versus the historical trend. The risk to local bond supply is balanced: government revenue could surprise on the upside thanks to growth while expenditure could increase if the Covid situation deteriorates. China should see more bond issuance to support growth.

相关报告

国际投行报告-全球芯片行业:芯片的冲突-台积电、三星和英特尔(英)

4445

类型:行研

上传时间:2022-06

标签:投行报告、芯片、冲突)

语言:英文

金额:5积分

HSBC-中国房地产和物业管理行业2022年展望-2021.11.9-75页

3787

类型:行研

上传时间:2021-11

标签:投行报告、房地产、物业)

语言:英文

金额:5积分

汇丰-中国汽车芯片

3694

类型:行研

上传时间:2022-07

标签:汽车、芯片、投行报告)

语言:英文

金额:5积分

HSBC-全球投资策略之未来城市:城市化形态的变化-2021.4-54页

2666

类型:策略

上传时间:2021-05

标签:投行报告、未来城市、城市化)

语言:英文

金额:5积分

瑞信-2021年全球财富报告(英)

2543

类型:专题

上传时间:2021-06

标签:全球财富、投行报告)

语言:英文

金额:5积分

瑞信-2022全球投资展望:股票、地区和宏观-2021.11.17-194页

1890

类型:宏观

上传时间:2021-11

标签:投行报告、2022投资展望、宏观经济)

语言:英文

金额:5积分

瑞信-全球半导体行业:中国集成电路产业的不均衡崛起-2021.1.20-184页

1736

类型:行研

上传时间:2021-01

标签:半导体、中国集成电路、投行报告)

语言:英文

金额:5积分

瑞信-全球财富报告2020-2020.10-56页

1699

类型:专题

上传时间:2020-10

标签:全球财富、投行报告)

语言:英文

金额:5积分

瑞信-中国能源行业-中国氢能源:如何更好地发挥中国氢主题-2021.3.15-118页

1536

类型:行研

上传时间:2021-03

标签:能源、氢能源、投行报告)

语言:英文

金额:5积分

中国投资策略之2021年中国的十大问题-2021.1.8-36页

1445

类型:策略

上传时间:2021-01

标签:中国投资、2021、投行报告)

语言:英文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册