微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

Numerical growth target: Will it be abandoned?

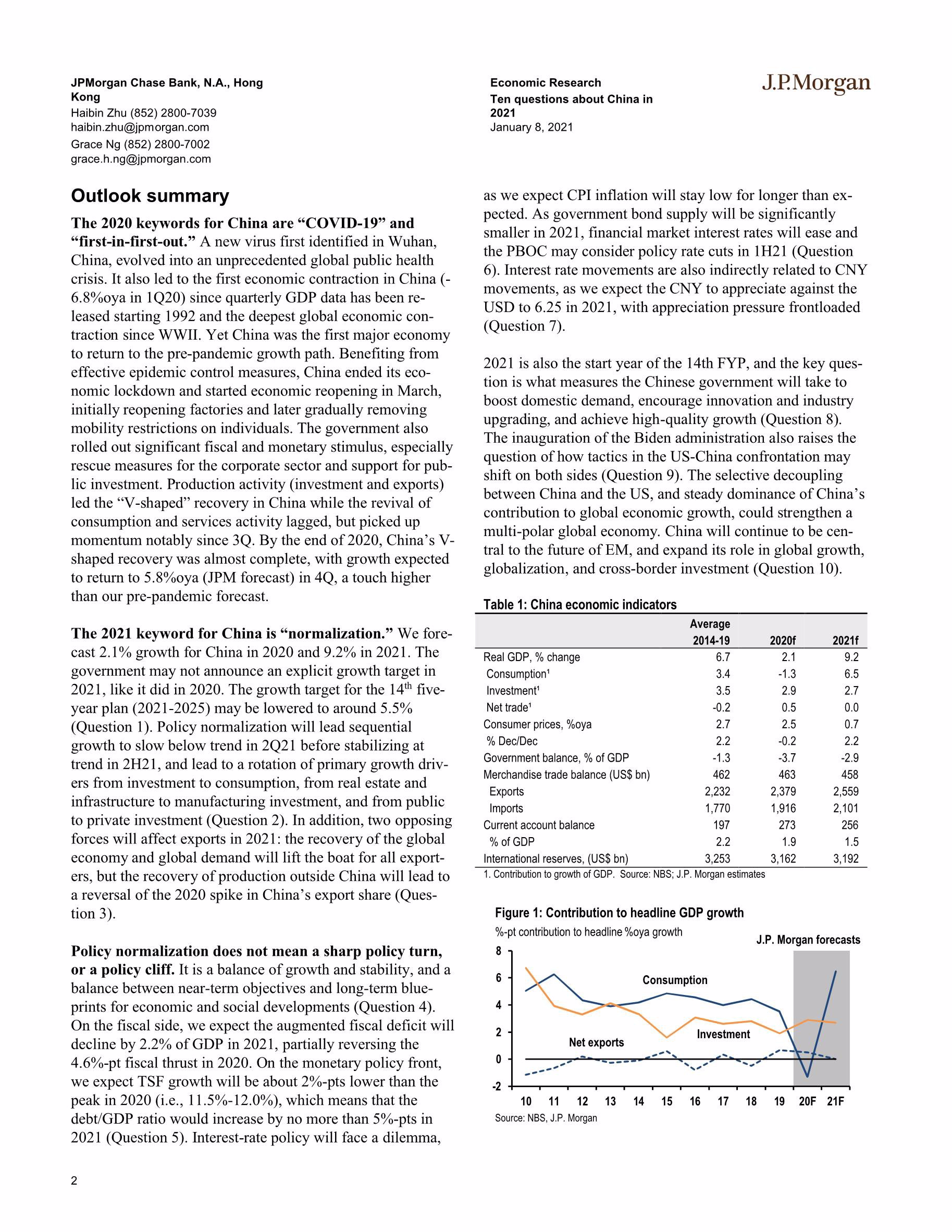

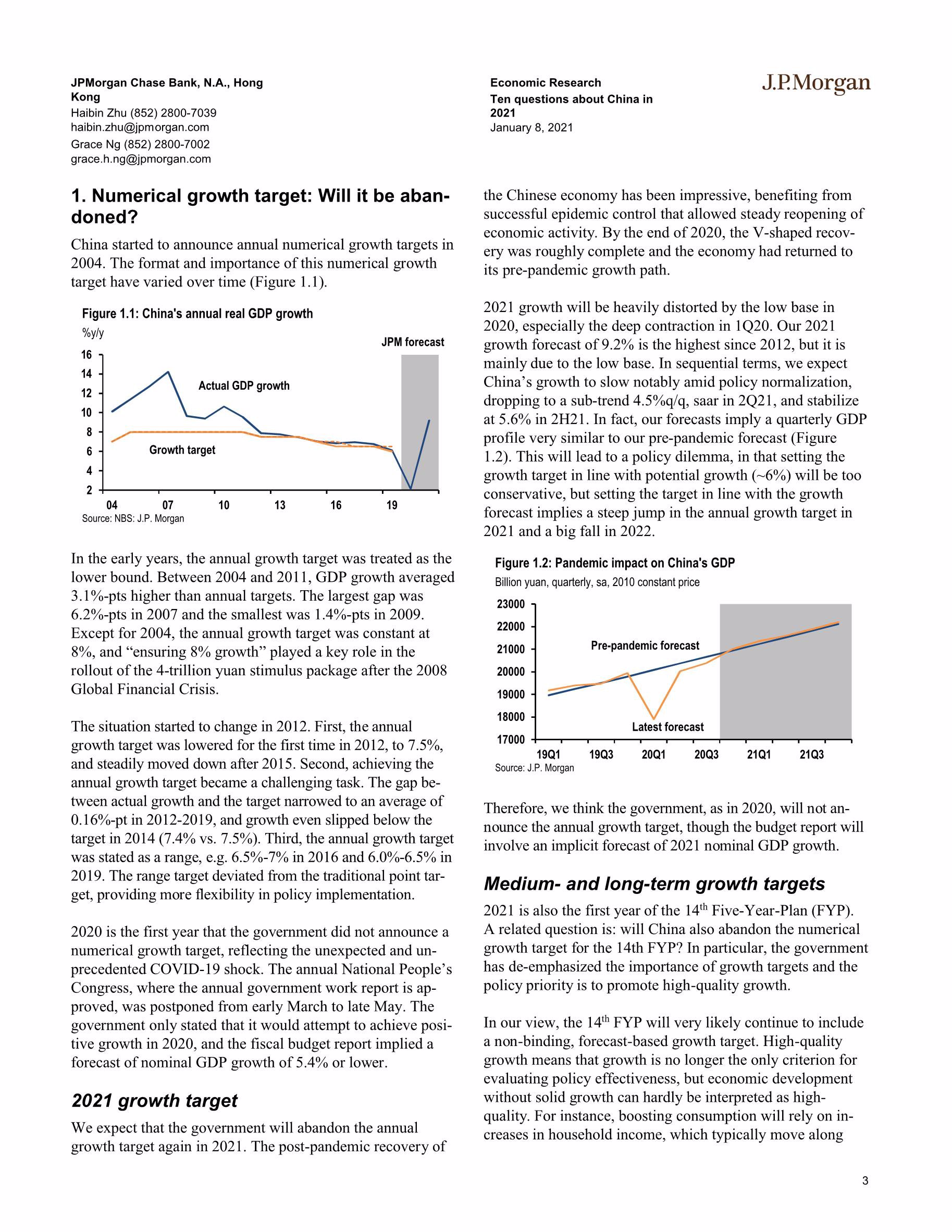

We expect the government will not announce a numerical growth target for 2021, like it did in 2020. We forecast China’s 2021 growth at 9.2%, and that China will match the size of the US economy around 2030.

What are primary growth drivers in 2021?

With the recovery of household income, successful pandemic control, and vaccine availability, we expect a growth rotation from investment to consumption and from manufacturing to services in 2021.

China’s export share spiked in 2020. Will it continue in 2021?

Solid global recovery in 2021 should boost demand for Chinese exports, though normalization in global production may lead to moderate correction in China’s world export share to around 15%.

What to expect from policy normalization?

Policy normalization includes modest fiscal consolidation (a fiscal drag of 2.2% of GDP), a credit slowdown (lower TSF growth by ~2%-pts), the end of regulatory forbearance, and debt stabilization efforts.

Will deleveraging efforts trigger credit stress?

No, we think the policy will find a balance between market discipline and financial stability. Risks are misinterpretation and over-execution in policy implementation.

Why we expect lower interest rates?

Our non-consensus forecast of lower interest rates is based on our forecast of low inflation and weak reflationary momentum, reduced supply of government bonds, debt burden, and CNY appreciation pressure.

Will CNY appreciation continue into 2021? .

Solid current account surplus, favorable interest rate differentials, and diminished risks of tariff escalation under a Biden administration suggest the CNY will appreciate to 6.25 against the USD in 2021, with the appreciation pressure frontloaded in 1H21.

How will the 14th Five-Year-Plan shore up domestic loop?

Dual circulation is based on further reform and openness. Areas of opportunity include consumption upgrading, innovations, digitalization of the economy, and green investment.

How will US-China relationship evolve?

The Biden administration will bring changes in tactics, and lower tail risk. Nonetheless, US-China super-power competition will continue, with limited areas of cooperation.

What is the role of China for EM?

China will continue to expand its role in global growth, globalization, and cross-border investment. China will continue to be central to the future of EM.

相关报告

国际投行报告-全球芯片行业:芯片的冲突-台积电、三星和英特尔(英)

4434

类型:行研

上传时间:2022-06

标签:投行报告、芯片、冲突)

语言:英文

金额:5积分

HSBC-中国房地产和物业管理行业2022年展望-2021.11.9-75页

3780

类型:行研

上传时间:2021-11

标签:投行报告、房地产、物业)

语言:英文

金额:5积分

汇丰-中国汽车芯片

3678

类型:行研

上传时间:2022-07

标签:汽车、芯片、投行报告)

语言:英文

金额:5积分

HSBC-全球投资策略之未来城市:城市化形态的变化-2021.4-54页

2660

类型:策略

上传时间:2021-05

标签:投行报告、未来城市、城市化)

语言:英文

金额:5积分

世界经济论坛:2021全球风险报告(英文版)

2653

类型:宏观

上传时间:2021-01

标签:全球风险、2021)

语言:英文

金额:5积分

瑞信-2021年全球财富报告(英)

2541

类型:专题

上传时间:2021-06

标签:全球财富、投行报告)

语言:英文

金额:5积分

WTO-2021年世界贸易统计评论

2095

类型:专题

上传时间:2021-08

标签:WTO、2021、世界贸易)

语言:英文

金额:5积分

瑞信-2022全球投资展望:股票、地区和宏观-2021.11.17-194页

1885

类型:宏观

上传时间:2021-11

标签:投行报告、2022投资展望、宏观经济)

语言:英文

金额:5积分

瑞信-全球半导体行业:中国集成电路产业的不均衡崛起-2021.1.20-184页

1724

类型:行研

上传时间:2021-01

标签:半导体、中国集成电路、投行报告)

语言:英文

金额:5积分

瑞信-全球财富报告2020-2020.10-56页

1689

类型:专题

上传时间:2020-10

标签:全球财富、投行报告)

语言:英文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册