微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

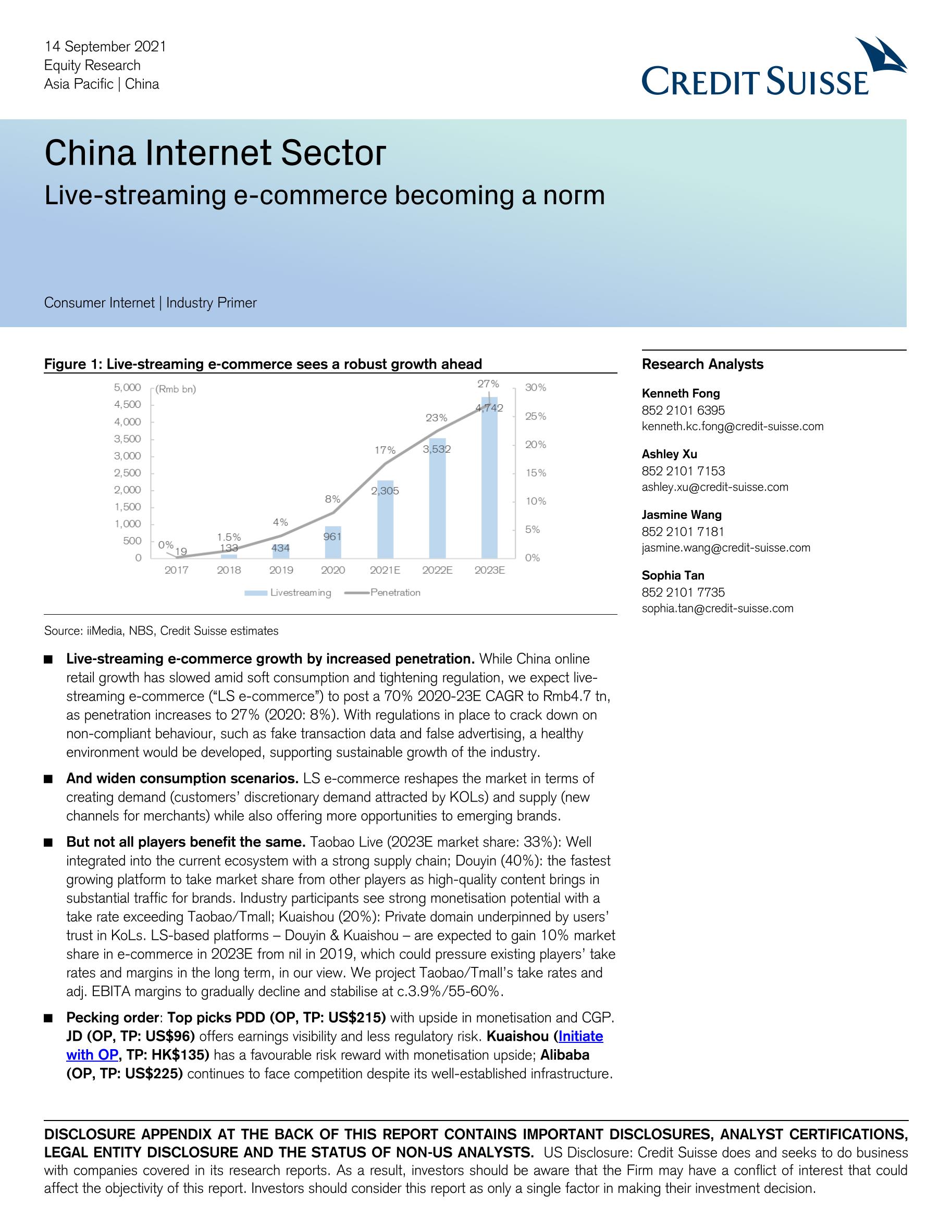

Live-streaming e-commerce growth by increased penetration. While China online retail growth has slowed amid soft consumption and tightening regulation, we expect live-streaming e-commerce (“LS e-commerce”) to post a 70% 2020-23E CAGR to Rmb4.7 tn, as penetration increases to 27% (2020: 8%). With regulations in place to crack down on non-compliant behaviour, such as fake transaction data and false advertising, a healthy environment would be developed, supporting sustainable growth of the industry.

And widen consumption scenarios. LS e-commerce reshapes the market in terms of creating demand (customers’ discretionary demand attracted by KOLs) and supply (new channels for merchants) while also offering more opportunities to emerging brands.

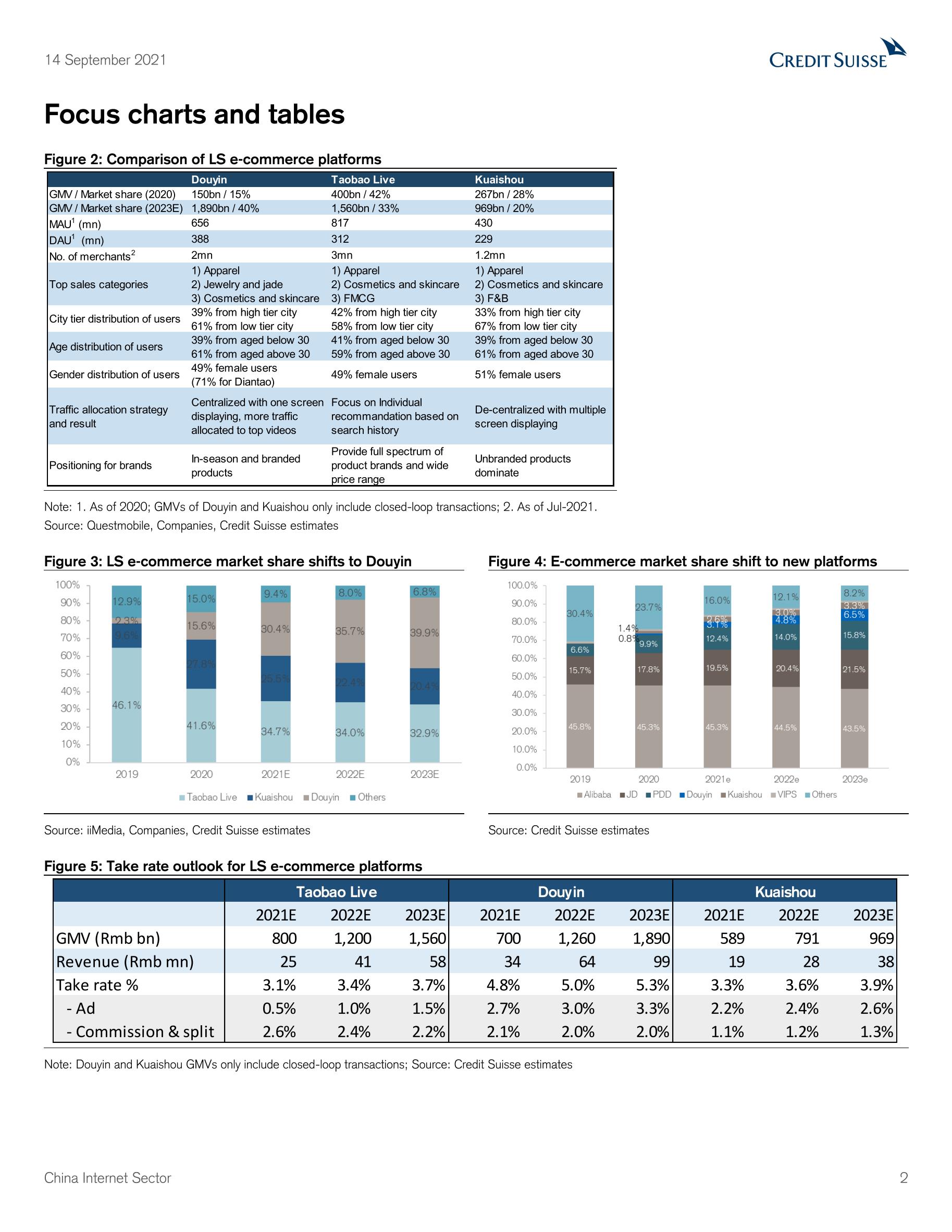

But not all players benefit the same. Taobao Live (2023E market share: 33%): Well integrated into the current ecosystem with a strong supply chain; Douyin (40%): the fastest growing platform to take market share from other players as high-quality content brings in substantial traffic for brands. Industry participants see strong monetisation potential with a take rate exceeding Taobao/Tmall; Kuaishou (20%): Private domain underpinned by users’ trust in KoLs. LS-based platforms – Douyin & Kuaishou – are expected to gain 10% market share in e-commerce in 2023E from nil in 2019, which could pressure existing players’ take rates and margins in the long term, in our view. We project Taobao/Tmall’s take rates and adj. EBITA margins to gradually decline and stabilise at c.3.9%/55-60%. Pecking order: Top picks PDD (OP, TP: US$215) with upside in monetisation and CGP. JD (OP, TP: US$96) offers earnings visibility and less regulatory risk. Kuaishou (Initiate with OP, TP: HK$135) has a favourable risk reward with monetisation upside; Alibaba (OP, TP: US$225) continues to face competition despite its well-established infrastructure.

相关报告

国际投行报告-全球芯片行业:芯片的冲突-台积电、三星和英特尔(英)

4445

类型:行研

上传时间:2022-06

标签:投行报告、芯片、冲突)

语言:英文

金额:5积分

HSBC-中国房地产和物业管理行业2022年展望-2021.11.9-75页

3787

类型:行研

上传时间:2021-11

标签:投行报告、房地产、物业)

语言:英文

金额:5积分

汇丰-中国汽车芯片

3694

类型:行研

上传时间:2022-07

标签:汽车、芯片、投行报告)

语言:英文

金额:5积分

HSBC-全球投资策略之未来城市:城市化形态的变化-2021.4-54页

2666

类型:策略

上传时间:2021-05

标签:投行报告、未来城市、城市化)

语言:英文

金额:5积分

瑞信-2021年全球财富报告(英)

2543

类型:专题

上传时间:2021-06

标签:全球财富、投行报告)

语言:英文

金额:5积分

瑞信-2022全球投资展望:股票、地区和宏观-2021.11.17-194页

1890

类型:宏观

上传时间:2021-11

标签:投行报告、2022投资展望、宏观经济)

语言:英文

金额:5积分

瑞信-全球半导体行业:中国集成电路产业的不均衡崛起-2021.1.20-184页

1736

类型:行研

上传时间:2021-01

标签:半导体、中国集成电路、投行报告)

语言:英文

金额:5积分

瑞信-全球财富报告2020-2020.10-56页

1699

类型:专题

上传时间:2020-10

标签:全球财富、投行报告)

语言:英文

金额:5积分

瑞信-中国能源行业-中国氢能源:如何更好地发挥中国氢主题-2021.3.15-118页

1536

类型:行研

上传时间:2021-03

标签:能源、氢能源、投行报告)

语言:英文

金额:5积分

中国投资策略之2021年中国的十大问题-2021.1.8-36页

1445

类型:策略

上传时间:2021-01

标签:中国投资、2021、投行报告)

语言:英文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册