微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

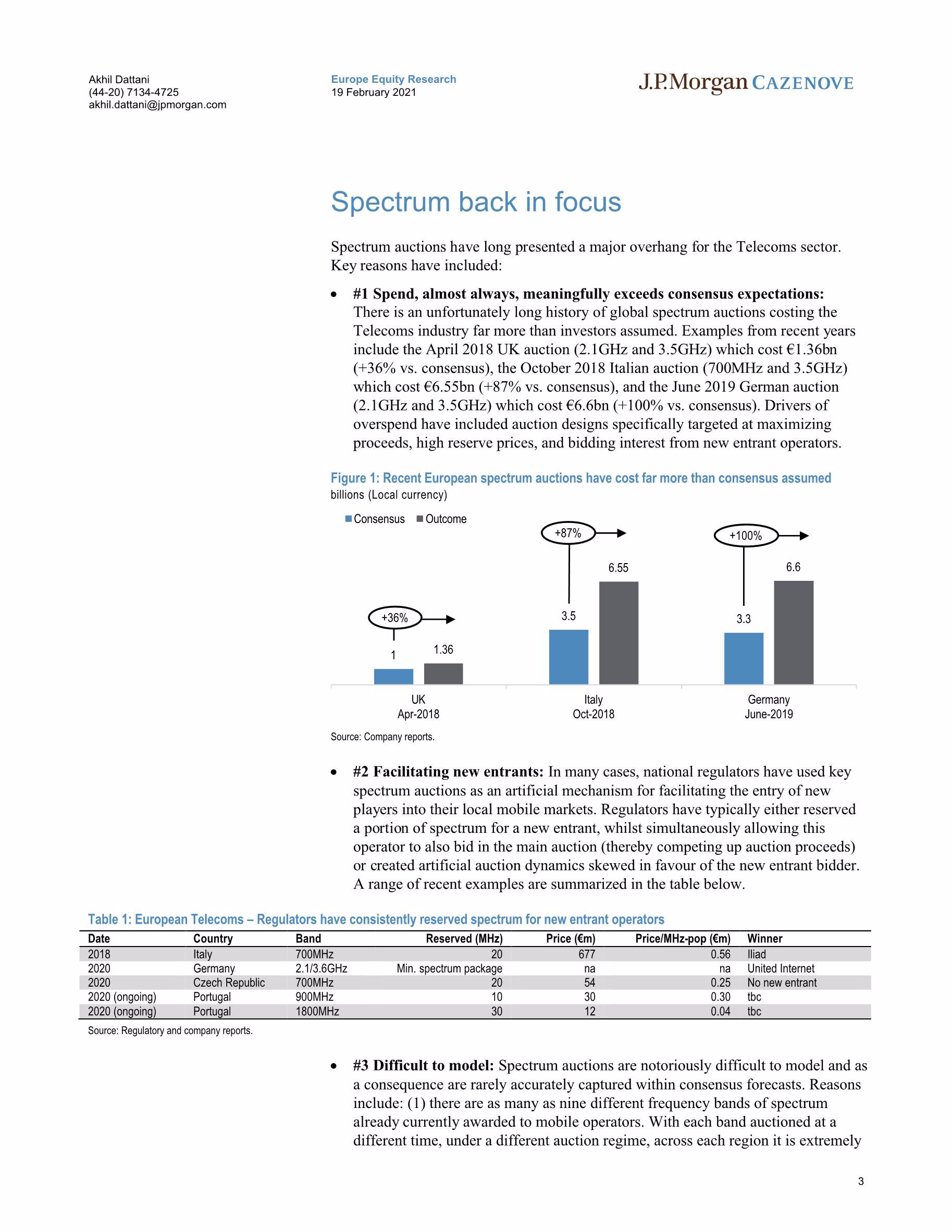

Spectrum has long been a sector curse. History is littered with examples of auctions that have either cost substantially more than expected, or facilitated new entrant competition. Recent newsflow only reinforces these themes. The US C-band auction has soared to $96bn (3x consensus), and the Portuguese auction will foster a new challenger. With our analysis identifying 28 additional global auctions on the horizon, and €52bn in spend, investors would be forgiven for questioning our contrarian 2021 sector OW. But we stay the course. Note: (1) 2021-22E global spend at €134bn (€30bn ex US), translates to “just” €33bn (€14bn ex US) for the Euro incumbents; (2) Helpfully, several EM regulators have altered policy objectives away from maximizing auction proceeds; (3) In Europe we expect auctions in Spain and the Nordics to prove benign, with only the UK competitive; (4) At a stock level, we alter 2020-22E spectrum spend assumptions for DT (+€10bn to €22.5bn due to the US), Telenor (+NOK8bn to NOK17.5bn due to DTAC), Vodafone (-€0.8bn to €4.7bn due to SA/Turkey), and Telefonica (-€0.7bn to €3.0bn due to Latam, though offset by higher capex).

US C-band (3.5GHz): Auction results are expected imminently with spend set to hit $96bn (3x consensus). We believe the “over-spend” is market specific, and should not be extrapolated. We have long argued consensus incorrectly forecasts US auctions with half an eye to European Price/Mhzpop benchmarks, failing to adequately adjust for differences in license duration (US perpetual vs Europe 15 years) or industry profitability (US sector EV is 4x Europe). For DT, C-band pricing serves to underscore the value of the 150Mhz of 2.5Ghz spectrum it gained through the $59bn Sprint acquisition (worth $31bn even if we assume a 40% discount to C-band).

Portuguese new entrant: 563MHz of spectrum is being sold across various bands. Frustratingly 40MHz is reserved for a confirmed new entrant (at odds with the depressed nature of industry returns). Whilst disappointing, note attempts to promote a new entrant in Czech failed, and in Germany states are proposing free licenses in return for coverage commitments.

€134bn in spend across 31 auctions: Our detailed bottom up, country by country modelling, leads us to forecast €134bn in 2021-22E spectrum spend across 31 global auctions. 78% (€104bn) of this is attributable to the US. By contrast European spend at €7bn (2021E) is only in-line with the 2019 level, and even this is only due to auction delayed from 2020E due to COVID-19.

Stock implications: We forecast €33bn of spectrum spend across the Euro Telco incumbents. We alter 2020-22E assumptions for DT (+€10bn to €23.5bn due to 2022E US auctions), Telenor (+NOK8bn to NOK17.5bn due to Thailand), Vodafone (-€0.8bn to €4.7bn due to more benign expectations across SA/Turkey) and Telefonica (-€0.7bn to €3.0bn due to Brazil where cash payments will be small, and the rest paid in capex commitments).

相关报告

国际投行报告-全球芯片行业:芯片的冲突-台积电、三星和英特尔(英)

4445

类型:行研

上传时间:2022-06

标签:投行报告、芯片、冲突)

语言:英文

金额:5积分

HSBC-中国房地产和物业管理行业2022年展望-2021.11.9-75页

3787

类型:行研

上传时间:2021-11

标签:投行报告、房地产、物业)

语言:英文

金额:5积分

汇丰-中国汽车芯片

3694

类型:行研

上传时间:2022-07

标签:汽车、芯片、投行报告)

语言:英文

金额:5积分

HSBC-全球投资策略之未来城市:城市化形态的变化-2021.4-54页

2667

类型:策略

上传时间:2021-05

标签:投行报告、未来城市、城市化)

语言:英文

金额:5积分

瑞信-2021年全球财富报告(英)

2543

类型:专题

上传时间:2021-06

标签:全球财富、投行报告)

语言:英文

金额:5积分

瑞信-2022全球投资展望:股票、地区和宏观-2021.11.17-194页

1890

类型:宏观

上传时间:2021-11

标签:投行报告、2022投资展望、宏观经济)

语言:英文

金额:5积分

瑞信-全球半导体行业:中国集成电路产业的不均衡崛起-2021.1.20-184页

1736

类型:行研

上传时间:2021-01

标签:半导体、中国集成电路、投行报告)

语言:英文

金额:5积分

瑞信-全球财富报告2020-2020.10-56页

1699

类型:专题

上传时间:2020-10

标签:全球财富、投行报告)

语言:英文

金额:5积分

瑞信-中国能源行业-中国氢能源:如何更好地发挥中国氢主题-2021.3.15-118页

1536

类型:行研

上传时间:2021-03

标签:能源、氢能源、投行报告)

语言:英文

金额:5积分

中国投资策略之2021年中国的十大问题-2021.1.8-36页

1445

类型:策略

上传时间:2021-01

标签:中国投资、2021、投行报告)

语言:英文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册