微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

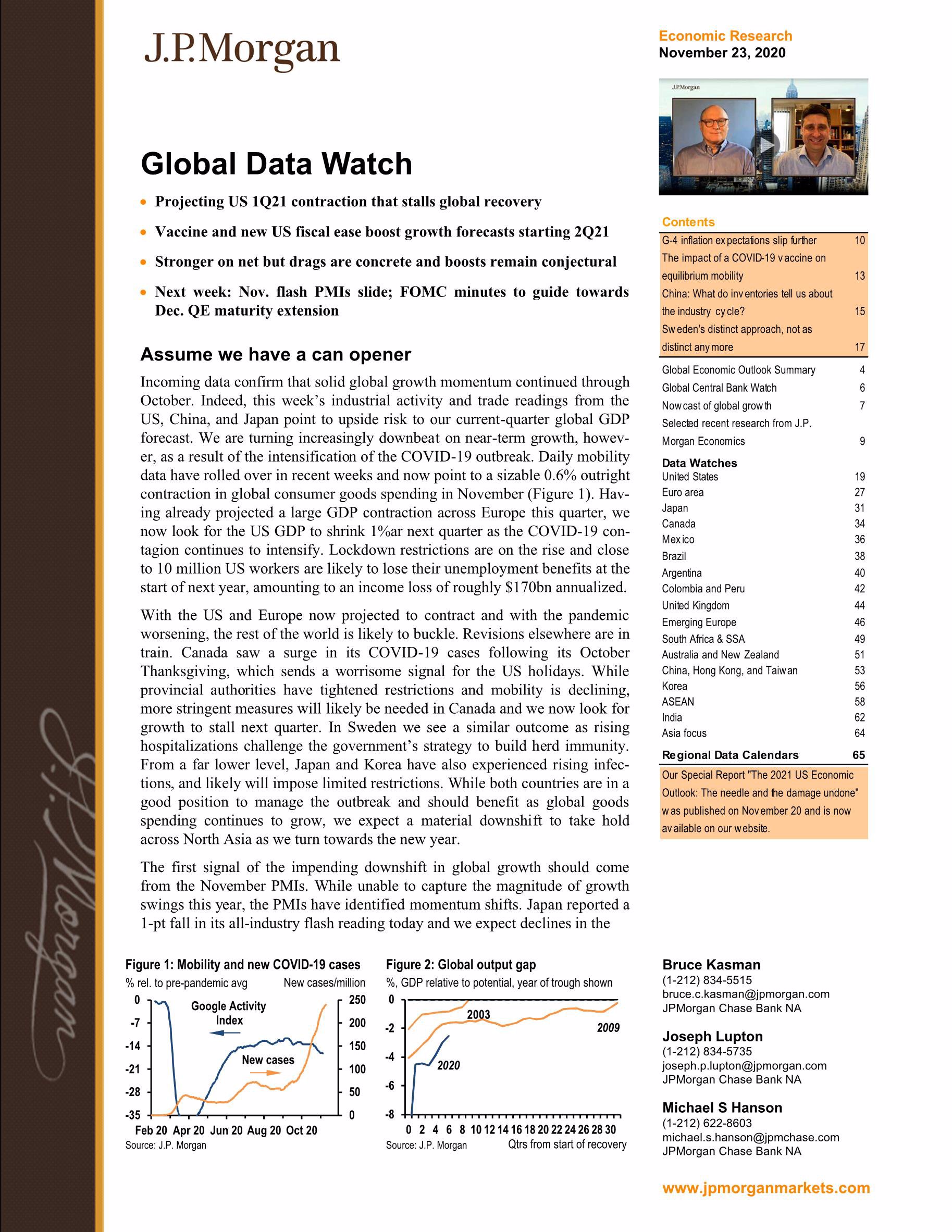

Incoming data confirm that solid global growth momentum continued throughOctober. Indeed, this week’s industrial activity and trade readings from theUS, China, and Japan point to upside risk to our current-quarter global GDPforecast. We are turning increasingly downbeat on near-term growth, however,as a result of the intensification of the COVID-19 outbreak. Daily mobilitydata have rolled over in recent weeks and now point to a sizable 0.6% outrightcontraction in global consumer goods spending in November (Figure 1). Havingalready projected a large GDP contraction across Europe this quarter, wenow look for the US GDP to shrink 1%ar next quarter as the COVID-19 contagioncontinues to intensify. Lockdown restrictions are on the rise and closeto 10 million US workers are likely to lose their unemployment benefits at thestart of next year, amounting to an income loss of roughly $170bn annualized.

With the US and Europe now projected to contract and with the pandemicworsening, the rest of the world is likely to buckle. Revisions elsewhere are intrain. Canada saw a surge in its COVID-19 cases following its OctoberThanksgiving, which sends a worrisome signal for the US holidays. Whileprovincial authorities have tightened restrictions and mobility is declining,more stringent measures will likely be needed in Canada and we now look forgrowth to stall next quarter. In Sweden we see a similar outcome as risinghospitalizations challenge the government’s strategy to build herd immunity.From a far lower level, Japan and Korea have also experienced rising infections,and likely will impose limited restrictions. While both countries are in agood position to manage the outbreak and should benefit as global goodsspending continues to grow, we expect a material downshift to take holdacross North Asia as we turn towards the new year.

The first signal of the impending downshift in global growth should comefrom the November PMIs.While unable to capture the magnitude of growthswings this year, the PMIs have identifiedmomentum shifts. Japan reported a 1-pt fall in its all-industry flash reading today and we expect declines in theother flash reports out on Monday, led by a 10-pt plunge inthe Euro area.

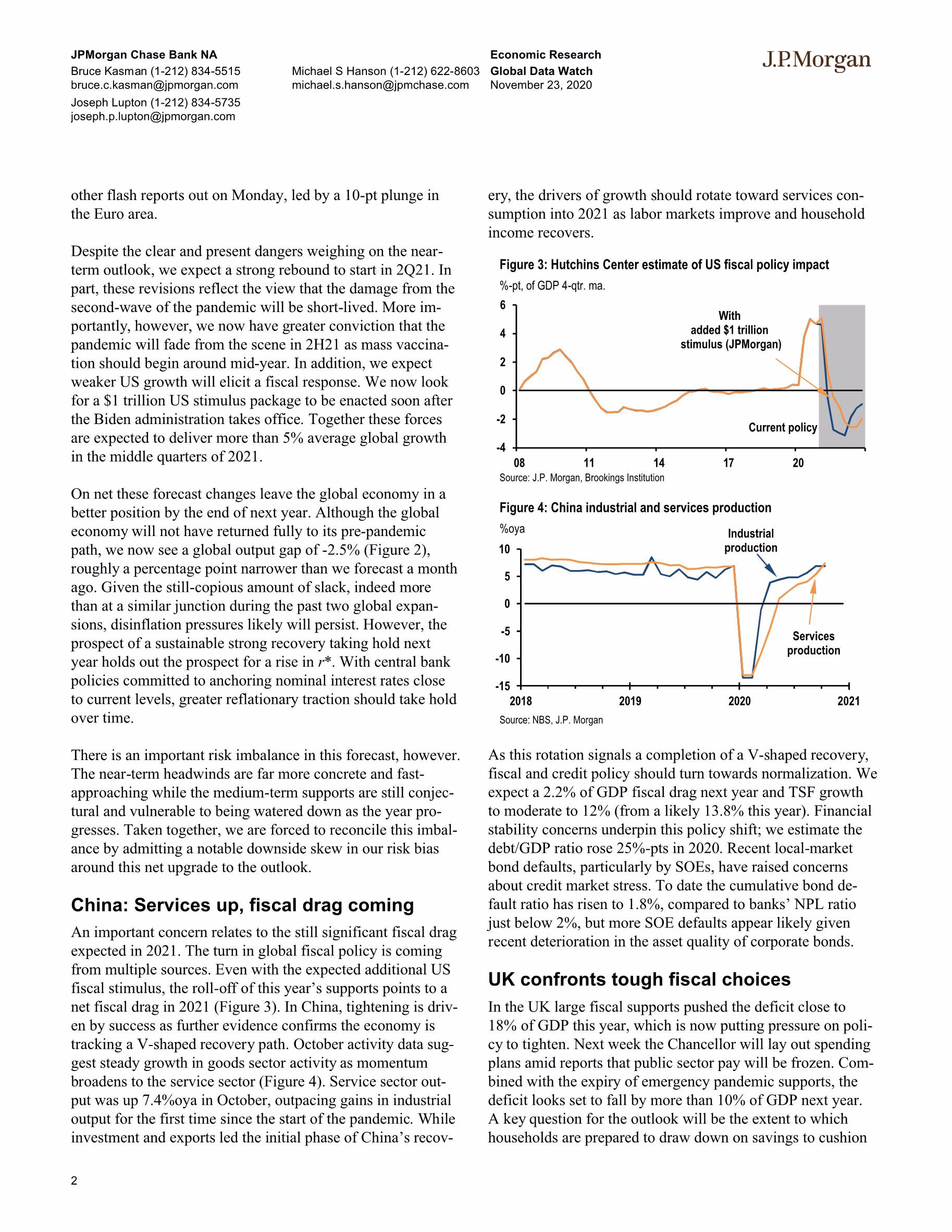

Despite the clear and present dangers weighing on the neartermoutlook, we expect a strong rebound to start in 2Q21. In part, these revisions reflect the view that the damage from the second-wave of the pandemic will be short-lived. More importantly, however, we now have greater conviction that the pandemic will fade from the scene in 2H21 as mass vaccination should begin around mid-year. In addition, we expect weaker US growth will elicit a fiscal response. We now look

for a $1 trillion US stimulus package to be enacted soon after the Biden administration takes office. Together these forces are expected to deliver more than 5% average global growth in the middle quarters of 2021.

相关报告

国际投行报告-全球芯片行业:芯片的冲突-台积电、三星和英特尔(英)

4390

类型:行研

上传时间:2022-06

标签:投行报告、芯片、冲突)

语言:英文

金额:5积分

HSBC-中国房地产和物业管理行业2022年展望-2021.11.9-75页

3753

类型:行研

上传时间:2021-11

标签:投行报告、房地产、物业)

语言:英文

金额:5积分

汇丰-中国汽车芯片

3652

类型:行研

上传时间:2022-07

标签:汽车、芯片、投行报告)

语言:英文

金额:5积分

HSBC-全球投资策略之未来城市:城市化形态的变化-2021.4-54页

2625

类型:策略

上传时间:2021-05

标签:投行报告、未来城市、城市化)

语言:英文

金额:5积分

瑞信-2021年全球财富报告(英)

2528

类型:专题

上传时间:2021-06

标签:全球财富、投行报告)

语言:英文

金额:5积分

瑞信-2022全球投资展望:股票、地区和宏观-2021.11.17-194页

1874

类型:宏观

上传时间:2021-11

标签:投行报告、2022投资展望、宏观经济)

语言:英文

金额:5积分

瑞信-全球半导体行业:中国集成电路产业的不均衡崛起-2021.1.20-184页

1690

类型:行研

上传时间:2021-01

标签:半导体、中国集成电路、投行报告)

语言:英文

金额:5积分

瑞信-全球财富报告2020-2020.10-56页

1674

类型:专题

上传时间:2020-10

标签:全球财富、投行报告)

语言:英文

金额:5积分

瑞信-中国能源行业-中国氢能源:如何更好地发挥中国氢主题-2021.3.15-118页

1519

类型:行研

上传时间:2021-03

标签:能源、氢能源、投行报告)

语言:英文

金额:5积分

中国投资策略之2021年中国的十大问题-2021.1.8-36页

1429

类型:策略

上传时间:2021-01

标签:中国投资、2021、投行报告)

语言:英文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册