微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

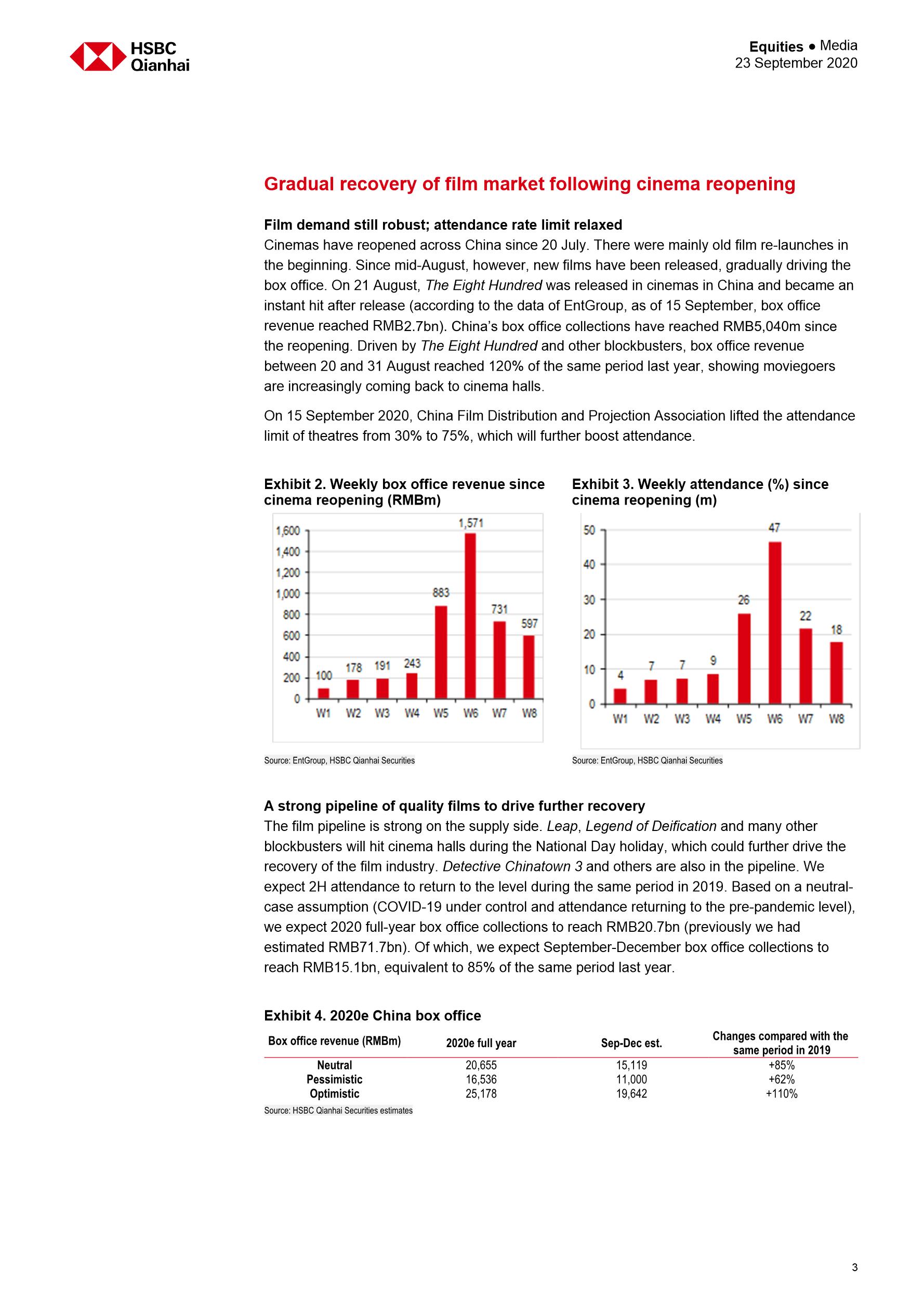

Box office warmed up by popular films. Cinemas have reopened across China since 20 July. The Eight Hundred and other films have hit the silver screen, boosting the box office gradually. China’s box office revenue has reached RMB5,040m since the reopening. Box office revenue between 20 and 31 August reached 120% of the same period last year, which shows that moviegoers are coming back to cinemas. On 15 September, China Film Projection Association lifted the attendance limit of theatres from 30% to 75%, and we think the new rule will further boost attendance.

Strong film pipeline at the supply side. Eyes on National Day holiday. Leap and Legend of Deification will hit cinema halls during the National Day holiday, which could further drive the film industry’s recovery. Besides, Detective Chinatown 3 and others are also in the pipeline. We expect 2020 box office to reach RMB20.7bn (previously we had estimated RMB71.7bn). Of which, we expect September-December box office to be RMB15.1bn, equivalent to 85% of the same period last year.

Industry reshuffled by COVID-19; we expect market share of industry leaders to grow. According to China Film Association, 42% of cinemas faced shutdown risks owing to the pandemic. But this gives industry leaders the opportunity to buck the trend by taking share from small cinemas. For instance, Wanda Film plans to add 162 cinemas, 1,258 screens and 176,000 seats in 2020-22. In 2019, China’s top three cinema lines had a total market share of 31%, far lower than 59% in the US. Long term, we see room for the market share of China’s leading cinemas to grow.

Film-related companies to enter recovery period. We stay optimistic about the outlook of the film industry, and believe the impact of the pandemic will be short-lived. We think demand for cinemas and high-quality films will stay intact. With blockbusters hitting the screen during the National Day holiday, we believe the film market will gradually recover. We maintain our Buy ratings on Wanda Film and China Film, and prefer Enlight Media, upgrading the stock to Buy from Hold. We also raise our TPs for all three stocks. Key downside risks: Resurgence of the pandemic, lower-thanexpected box office, and intensifying competition.

相关报告

国际投行报告-全球芯片行业:芯片的冲突-台积电、三星和英特尔(英)

4447

类型:行研

上传时间:2022-06

标签:投行报告、芯片、冲突)

语言:英文

金额:5积分

HSBC-中国房地产和物业管理行业2022年展望-2021.11.9-75页

3788

类型:行研

上传时间:2021-11

标签:投行报告、房地产、物业)

语言:英文

金额:5积分

汇丰-中国汽车芯片

3694

类型:行研

上传时间:2022-07

标签:汽车、芯片、投行报告)

语言:英文

金额:5积分

HSBC-全球投资策略之未来城市:城市化形态的变化-2021.4-54页

2667

类型:策略

上传时间:2021-05

标签:投行报告、未来城市、城市化)

语言:英文

金额:5积分

瑞信-2021年全球财富报告(英)

2543

类型:专题

上传时间:2021-06

标签:全球财富、投行报告)

语言:英文

金额:5积分

瑞信-2022全球投资展望:股票、地区和宏观-2021.11.17-194页

1891

类型:宏观

上传时间:2021-11

标签:投行报告、2022投资展望、宏观经济)

语言:英文

金额:5积分

瑞信-全球半导体行业:中国集成电路产业的不均衡崛起-2021.1.20-184页

1744

类型:行研

上传时间:2021-01

标签:半导体、中国集成电路、投行报告)

语言:英文

金额:5积分

瑞信-全球财富报告2020-2020.10-56页

1701

类型:专题

上传时间:2020-10

标签:全球财富、投行报告)

语言:英文

金额:5积分

瑞信-中国能源行业-中国氢能源:如何更好地发挥中国氢主题-2021.3.15-118页

1536

类型:行研

上传时间:2021-03

标签:能源、氢能源、投行报告)

语言:英文

金额:5积分

中国投资策略之2021年中国的十大问题-2021.1.8-36页

1445

类型:策略

上传时间:2021-01

标签:中国投资、2021、投行报告)

语言:英文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册