微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

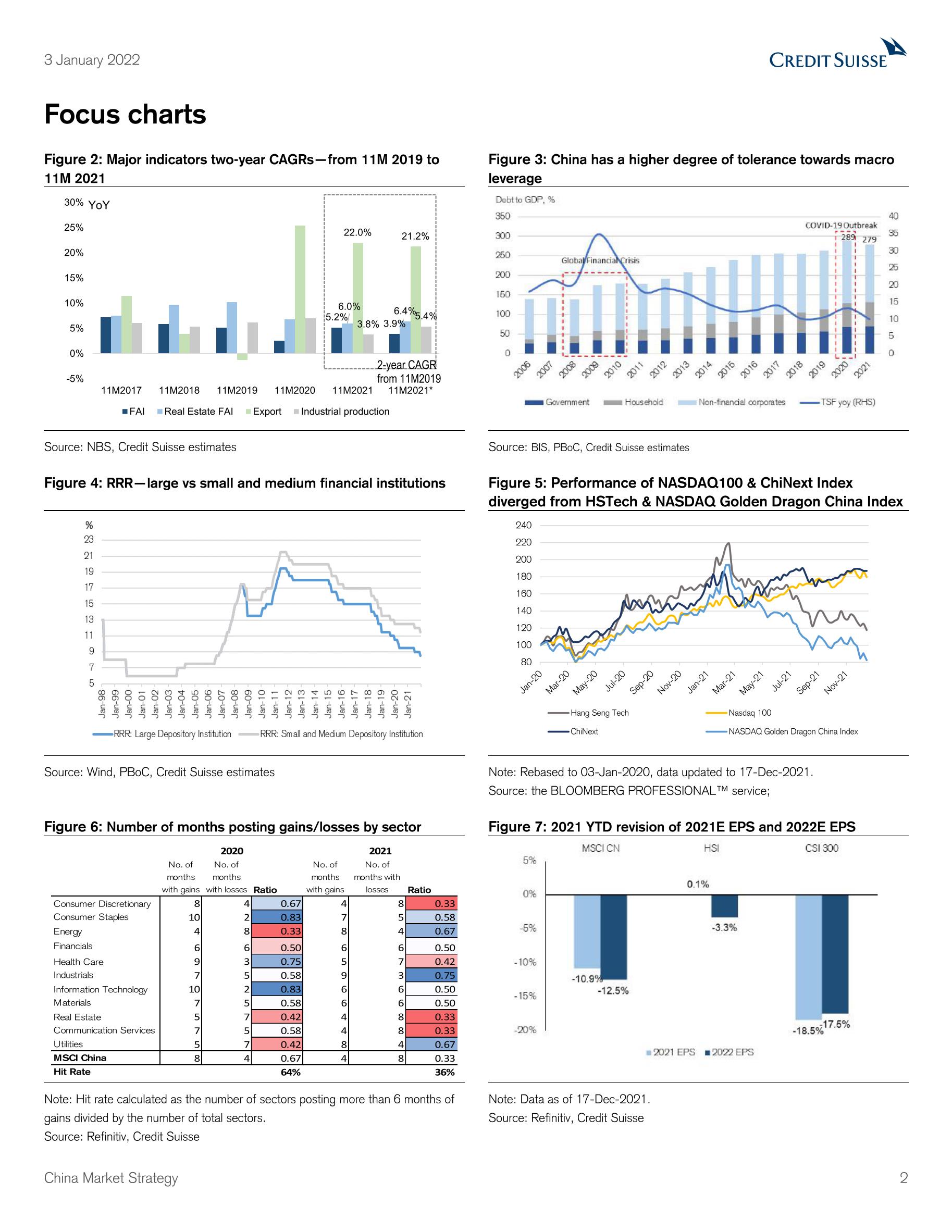

Macro economy set to bottom out. Following a V-shaped recovery in 2020, China’s growth lost momentum since 3Q21 due to resurging COVID, summer flooding, unexpected power cuts and property tightening. We expect to see moderate recovery in 2H22, after a still tough 1H22. We expect China to speed up fiscal expenditure, carry out a constructive monetary policy and adjust the implementation pace for China’s long-term development goals such as common prosperity and carbon neutrality.

On-the-ground checks suggest a mixed outlook. According to the CS CQi team’s industry and consumer surveys, property sales managers confirmed the moderate easing; material producers are still cautious on demand outlook and expect the high power tariffs to sustain for longer; private SME manufacturers are cautious about the year while service providers are more optimistic.

2022 to be a better year for stocks after correction. China and Hong Kong equity markets experienced remarkable corrections in 2021, with dramatic sector rotation. Sixteen out of 22 sectors declined, led by consumer services, Macau, software, insurance and real estate. Only 36% of sectors managed to achieve more positive monthly returns than negative in 2021, in sharp contrast to 64% in 2020. Downward revision of corporate earnings was also not helpful. However, the central government is swiftly taking action to stabilise the economy, and fine-tuning macro and industry policies accordingly, which sends a positive policy signal. We expect China’s equity market is set to recover, given positive policy direction, low investor expectation, and cheap valuation, despite a near-term slowing economy. Our new index targets for MSCI China/HSI/CSI300 are 91/26,200/5,760, offering 11.7%/13.4%/17.0% upsides respectively.

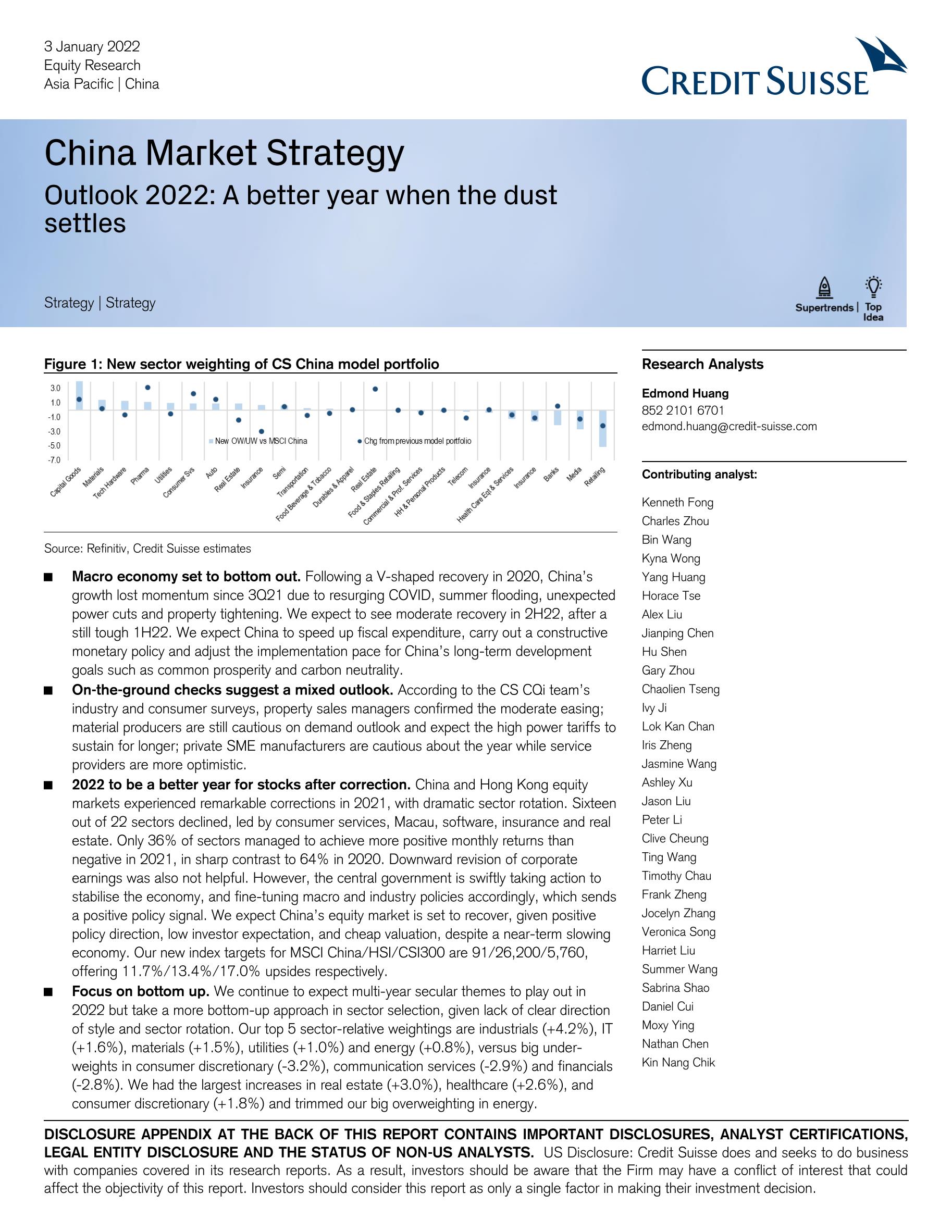

Focus on bottom up. We continue to expect multi-year secular themes to play out in 2022 but take a more bottom-up approach in sector selection, given lack of clear direction of style and sector rotation. Our top 5 sector-relative weightings are industrials (+4.2%), IT (+1.6%), materials (+1.5%), utilities (+1.0%) and energy (+0.8%), versus big under-weights in consumer discretionary (-3.2%), communication services (-2.9%) and financials (-2.8%). We had the largest increases in real estate (+3.0%), healthcare (+2.6%), and consumer discretionary (+1.8%) and trimmed our big overweighting in energy.

相关报告

瑞信-中国互联网行业2022年展望:在充满挑战的时代找到一线希望(英)

1156

类型:行研

上传时间:2022-02

标签:互联网行业、2022展望)

语言:英文

金额:5积分

《资本市场交易与中国投资策略 - 实践者指南》

1116

类型:电子书

上传时间:2020-10

标签:资本市场交易、中国投资策略)

语言:英文

金额:5积分

国际投行报告-中国投资策略-2022年中国经济展望:转折点-2021.11.14-22页

871

类型:宏观

上传时间:2021-11

标签:中国投资策略、投行报告、中国经济展望)

语言:英文

金额:5积分

HSBC-中国投资策略之牛年的中国:碳、货币和电子商务-2021.2-118页

766

类型:策略

上传时间:2021-03

标签:中国投资策略、碳、货币、电子商务)

语言:英文

金额:5积分

国际投行报告-全球投资策略-展望2022年:多资产方向-2021.10.7-38页

471

类型:策略

上传时间:2021-10

标签:投资策略、2022展望、国际投行)

语言:英文

金额:5积分

HSBC-中国投资策略-中国在岸市场洞察:如何去治疗一个生病的巨人-2021.6.1-34页

371

类型:策略

上传时间:2021-06

标签:中国投资策略、在岸市场)

语言:英文

金额:5积分

国际投行报告-中国投资策略-俄乌冲突:重新评估能源安全-2022.3.9-40页

240

类型:策略

上传时间:2022-03

标签:中国投资策略、投行报告、俄乌冲突)

语言:英文

金额:5积分

国际投行报告-中国投资策略-全球跨国公司中国信心指数(2021年第四季度):令人惊讶的反弹可能无法持续-2022.3.21-23页

229

类型:策略

上传时间:2022-03

标签:中国投资策略、全球跨国公司、国际投行报告)

语言:英文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册