微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

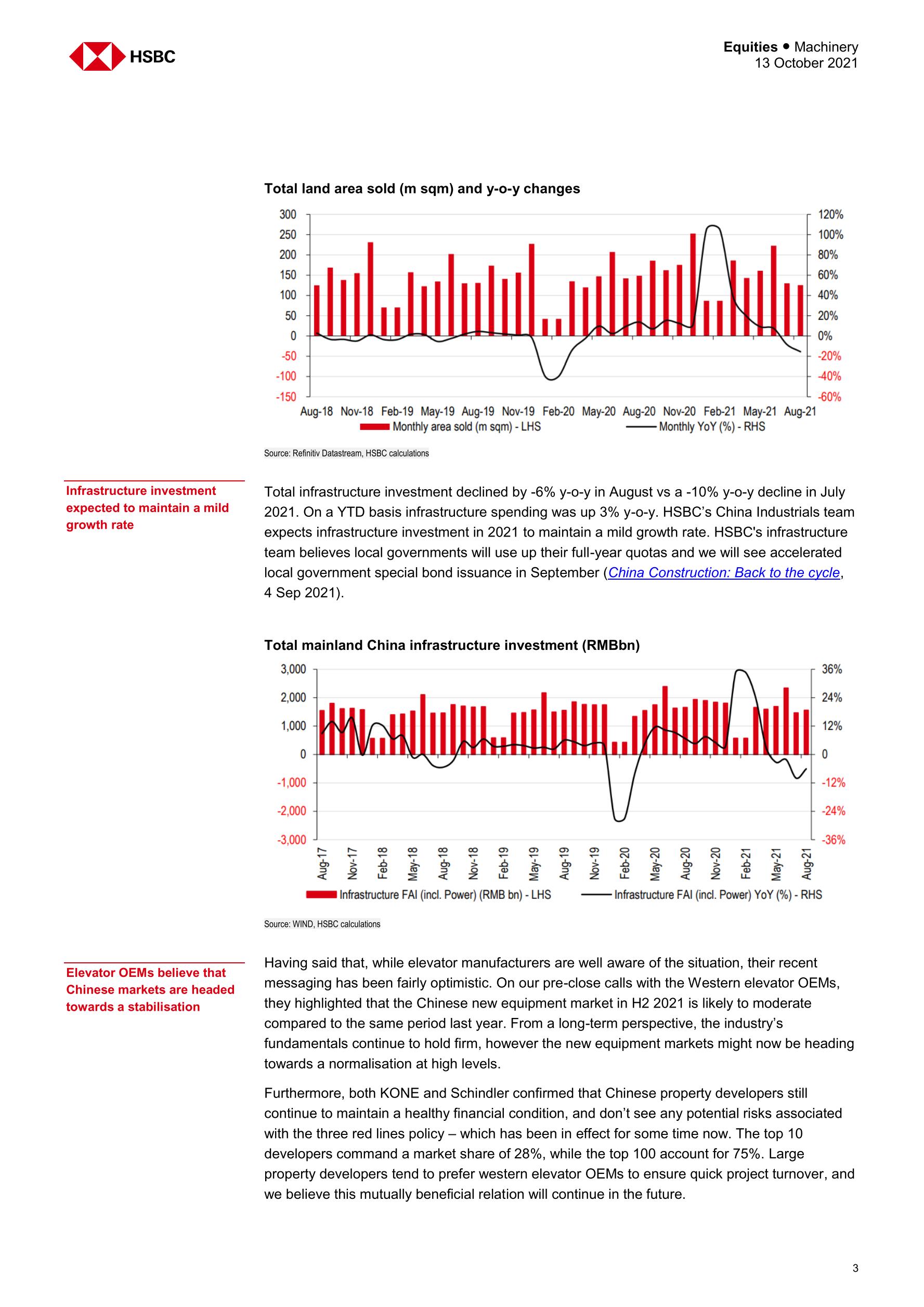

Trouble in the China real estate market post Evergrande; we quantify the risks for global OEMs with sensitivities Strong growth in the other markets, infra push and improvement in service should drive growth in the near term Long-term growth drivers intact; adjust forecasts and TPs, no change in ratings, maintain Buy on KONE and Canny Trouble ahead: China is the world’s largest new equipment market (with a c70% share in unit terms) for elevators and escalators, with residential real estate constituting the bulk of this demand. Restrictive policy measures, credit tightening and the Evergrande situation have put pressure on this important new equipment market and we quantify the risks associated with this weakness in China real estate for our elevators coverage.

However, we believe a strong outlook in other residential and commercial real estate markets combined with an infrastructure push across economies should limit the overall impact on new equipment growth. Further, a resilient maintenance business and a recovery in repairs and modernisation should help elevator OEMs to tide this crisis in the near term. Recent share price underperformance reflects the caution related to the China market and we show sensitivities on page 5.

Long-term growth drivers intact: Rapid urbanisation, growth of vertical cities, infrastructure development and the need for modernisation of existing buildings should continue to drive demand for elevators and escalators in the medium-long term.

Further, as highlighted in our earlier report, elevator OEMs are pushing for digitalisation, connecting their existing installed base, and the pace has accelerated post COVID-19 with the need for hygiene, safety and remote connectivity. We expect this rapid digitalisation to lead to additional digital services revenues, improved conversion and retention rates, and higher service efficiencies, resulting in additional organic growth of c1% and a margin improvement of c40-60 bps pa over the next 4-5 years. Elevator OEMs stand to benefit on the ESG front from connected elevators.

We adjust forecasts and TPs, maintain Buy on KONE and Canny Elevators: In this report, we cut our estimates for KONE, Schindler and Otis, incorporating the weakness in China real estate. KONE has underperformed its elevator peers over the past six months and China risk is more than priced in, which we consider unjustified given the underlying quality of its business. We cut our TPs for the three global OEMs.

相关报告

国际投行报告-全球芯片行业:芯片的冲突-台积电、三星和英特尔(英)

4446

类型:行研

上传时间:2022-06

标签:投行报告、芯片、冲突)

语言:英文

金额:5积分

HSBC-中国房地产和物业管理行业2022年展望-2021.11.9-75页

3788

类型:行研

上传时间:2021-11

标签:投行报告、房地产、物业)

语言:英文

金额:5积分

汇丰-中国汽车芯片

3694

类型:行研

上传时间:2022-07

标签:汽车、芯片、投行报告)

语言:英文

金额:5积分

HSBC-全球投资策略之未来城市:城市化形态的变化-2021.4-54页

2667

类型:策略

上传时间:2021-05

标签:投行报告、未来城市、城市化)

语言:英文

金额:5积分

瑞信-2021年全球财富报告(英)

2543

类型:专题

上传时间:2021-06

标签:全球财富、投行报告)

语言:英文

金额:5积分

HSBC-中国房地产:通过城市更新项目实现增长的新途径-2020.7.16-35页

1896

类型:行研

上传时间:2020-07

标签:中国房地产、城市更新、投行报告)

语言:英文

金额:5积分

瑞信-2022全球投资展望:股票、地区和宏观-2021.11.17-194页

1891

类型:宏观

上传时间:2021-11

标签:投行报告、2022投资展望、宏观经济)

语言:英文

金额:5积分

瑞信-全球半导体行业:中国集成电路产业的不均衡崛起-2021.1.20-184页

1737

类型:行研

上传时间:2021-01

标签:半导体、中国集成电路、投行报告)

语言:英文

金额:5积分

瑞信-全球财富报告2020-2020.10-56页

1701

类型:专题

上传时间:2020-10

标签:全球财富、投行报告)

语言:英文

金额:5积分

瑞信-中国能源行业-中国氢能源:如何更好地发挥中国氢主题-2021.3.15-118页

1536

类型:行研

上传时间:2021-03

标签:能源、氢能源、投行报告)

语言:英文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册