微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

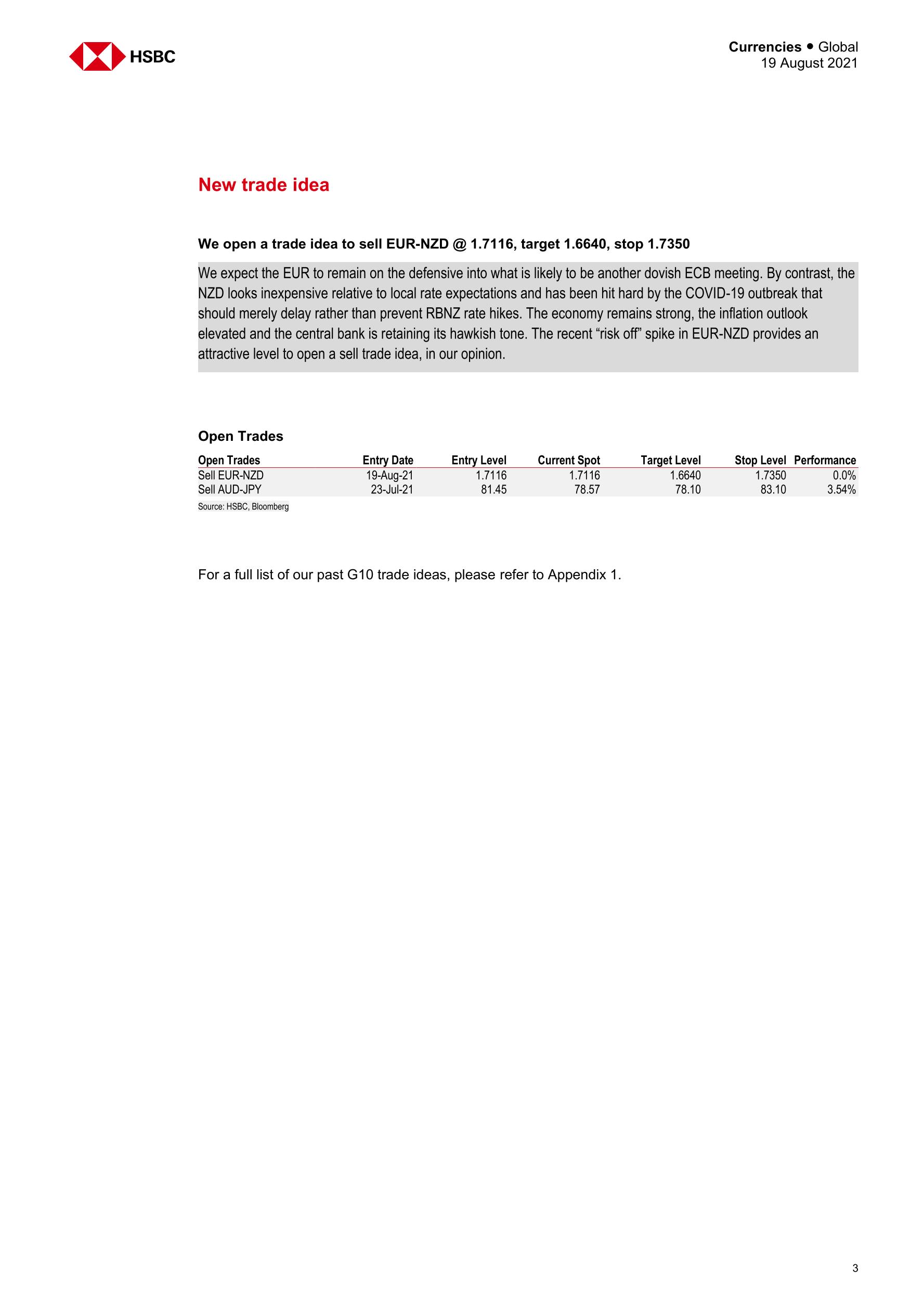

We continue to look for gradual USD strength with scope for an acceleration should the data permit EUR vulnerable on a number of fronts, but its negative yields and dovish ECB are likely to be more prominent for now Among the “risk on” currencies, from current levels we prefer the NZD over the AUD, CAD or Scandies Last month, we argued that a lack of good reasons to sell the dollar would be sufficient for it to grind higher. Our thinking is unchanged even as it posts new YTD highs (DXY index) and if anything, the risk might be for the move to accelerate. The key will be expectations for the 22 September FOMC in the context of the taper timing debate, but these may be shaped largely by August’s employment report on 3 September. Our forecast of a further grind higher in the USD does not rule out excitement. In addition, recent price action shows the USD is well placed to capitalize on any US data surprise, good or bad. Other currencies do not have this luxury.

For now, the EUR does not enjoy many luxuries at all. Growth is reviving as lockdowns ease, but low underlying inflation pressures and the headwinds of Delta variant uncertainties means this is unlikely to translate into any hawkish drift at the ECB’s September meeting that could hope to match the Fed’s taper debate. EUR-USD has tested beneath support at 1.17 and we expect the move lower to extend.

We suspect the better way to play a retreating EUR is not against the USD but against the NZD, which has been hit hard by a COVID-19 outbreak that looks likely to merely delay rather than derail the tightening. The currency looks inexpensive relative to those rate expectations and can play catch-up (with some carry) against the EUR.

Open a trade idea to sell EUR-NZD @ 1.7116, target 1.6640, stop 1.7350 We also expect the NZD to outpace other “risk on” currencies, such as the AUD, CAD and Scandies, which do not have the upside of a potential reprieve from COVID-19 repricing but do face the headwinds of global growth concerns and a Fed taper.

At the opposite end of the risk spectrum, the threat of SNB intervention is likely to become a bigger part of the CHF narrative, but we still see scope for EUR-CHF to grind lower unless 1.07 has become the “new 1.05” pain threshold for the central bank. USDJPY will remain beholden to the vagaries of 10Y US Treasury yields, which suggests a range environment, although the JPY crosses could still offer excitement. We retain our trade idea to sell AUD-JPY with a target of 78.10.

Finally, the GBP may have given up enough ground against the USD so long as UK data show the economy faring reasonably even as government support schemes are withdrawn. The main risk for the GBP would be a loss of enthusiasm from the speculative community, which has been an ardent buyer over the past couple of months.

相关报告

国际投行报告-全球芯片行业:芯片的冲突-台积电、三星和英特尔(英)

4447

类型:行研

上传时间:2022-06

标签:投行报告、芯片、冲突)

语言:英文

金额:5积分

HSBC-中国房地产和物业管理行业2022年展望-2021.11.9-75页

3788

类型:行研

上传时间:2021-11

标签:投行报告、房地产、物业)

语言:英文

金额:5积分

汇丰-中国汽车芯片

3695

类型:行研

上传时间:2022-07

标签:汽车、芯片、投行报告)

语言:英文

金额:5积分

研究所-如果美元失去了国际储备货币的地位会怎样?(中英对照)

2902

类型:宏观

上传时间:2023-08

标签:美元、国际储备货币、多极化)

语言:中英

金额:3元

HSBC-全球投资策略之未来城市:城市化形态的变化-2021.4-54页

2667

类型:策略

上传时间:2021-05

标签:投行报告、未来城市、城市化)

语言:英文

金额:5积分

瑞信-2021年全球财富报告(英)

2543

类型:专题

上传时间:2021-06

标签:全球财富、投行报告)

语言:英文

金额:5积分

美国智库-中国数字人民币!美元主导金融体系的替代方案

2409

类型:专题

上传时间:2021-09

标签:数字人民币、金融体系、美元)

语言:英文

金额:5积分

最新翻译10万字:美元的全球货币力量:问题与前景(中英文版)

2110

类型:宏观

上传时间:2023-02

标签:美元、人民币、金融危机)

语言:中文

金额:15元

瑞信-2022全球投资展望:股票、地区和宏观-2021.11.17-194页

1891

类型:宏观

上传时间:2021-11

标签:投行报告、2022投资展望、宏观经济)

语言:英文

金额:5积分

Financial Markets and Institutions《金融市场与金融机构》

1807

类型:电子书

上传时间:2020-08

标签:金融市场、金融机构、外汇)

语言:英文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册