微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

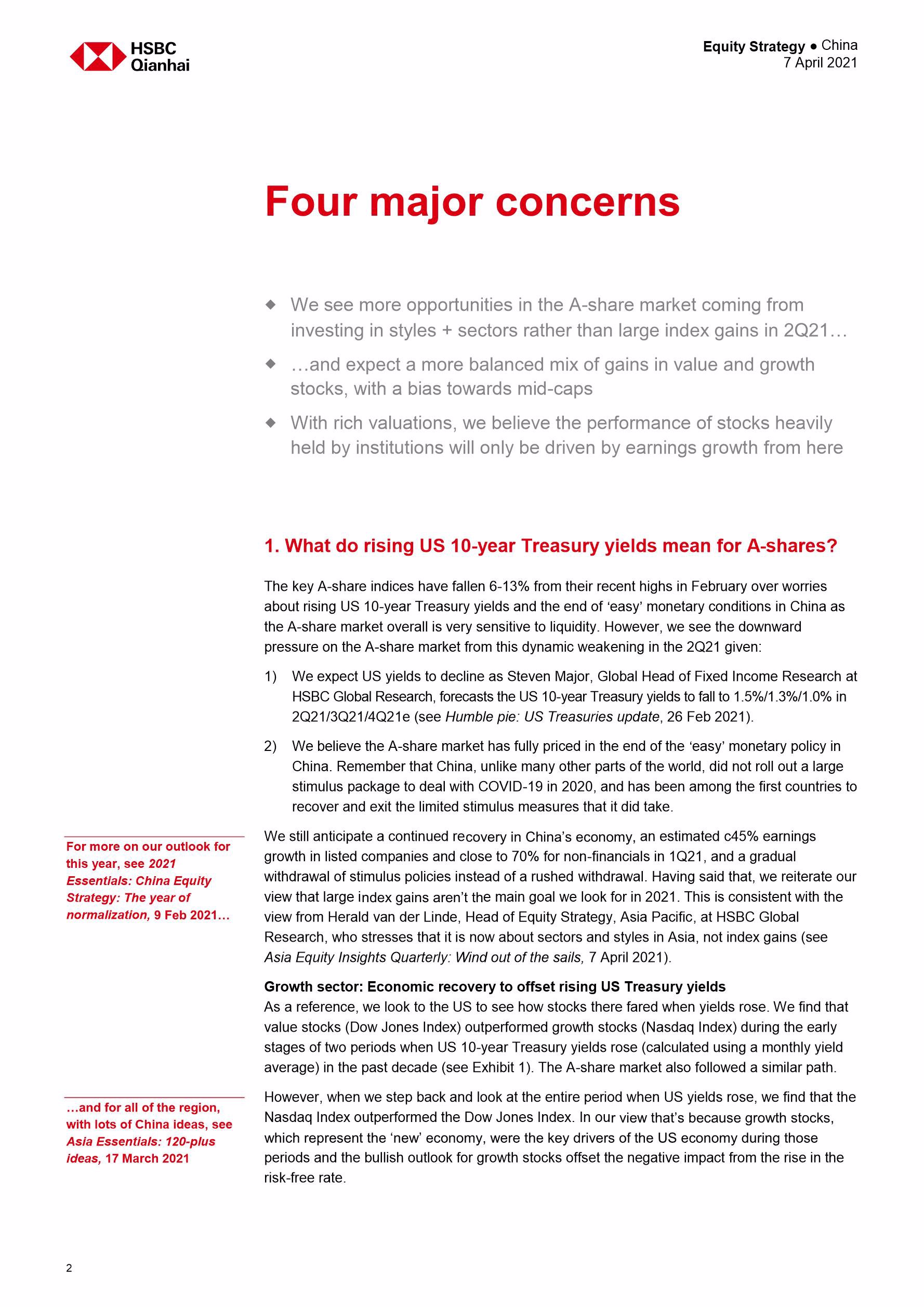

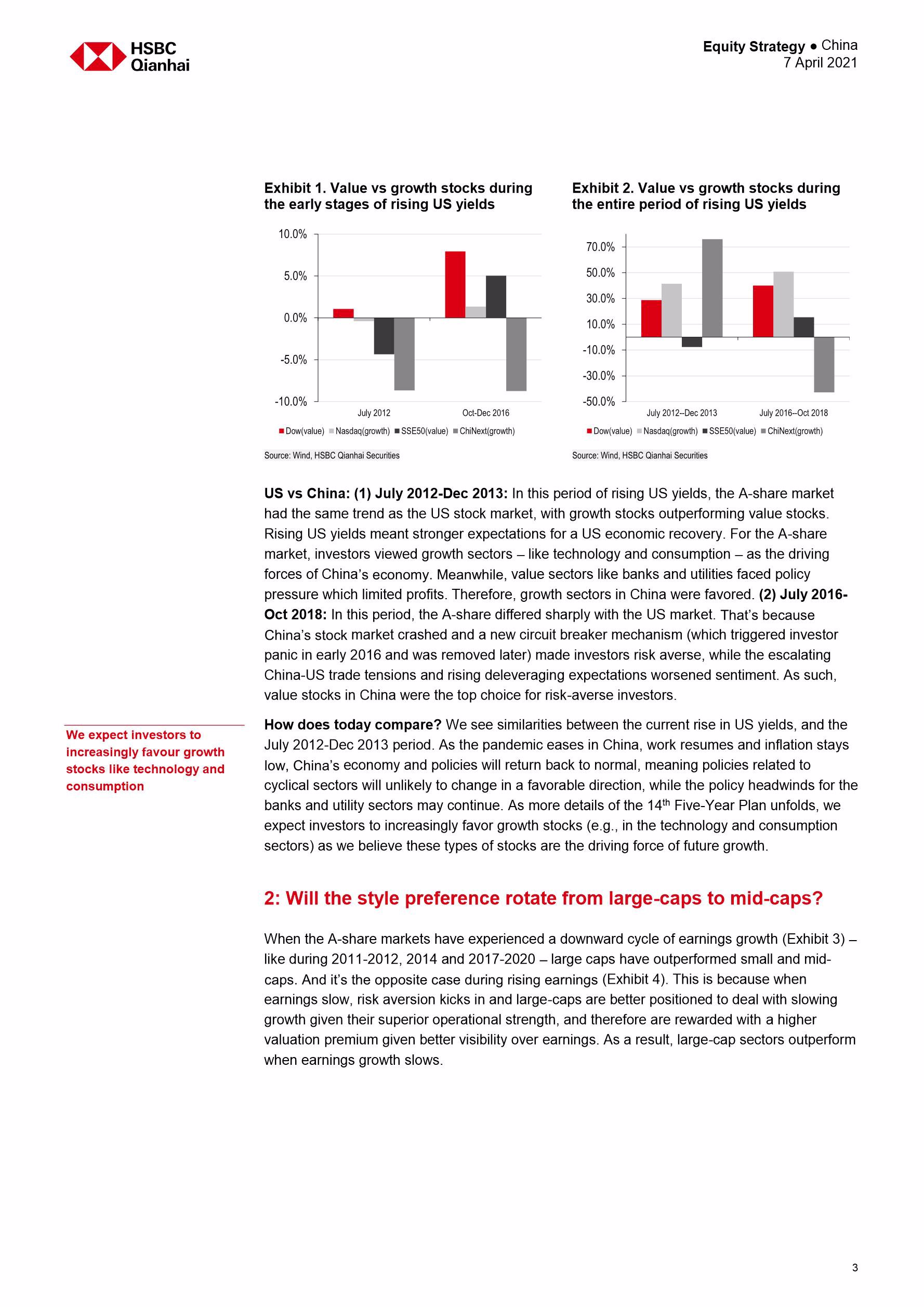

We see more opportunities in the A-share market coming from investing in styles + sectors in 2Q21; expect a mix of value and growth to outperform and a bias towards mid-caps We upgrade Cons Disc to overweight and downgrade Cons Staples and Healthcare to neutral; highlight 7 sub-sectors Present 10 mid-cap stocks with low PEG ratios + 12 bottomup ideas from IT, high-end manufacturing and consumption With the key A-share indices having fallen 6-13% since the highs reached in February, we address four major concerns from A-share investors: 1. What’s the impact of rising US yields? While higher Treasury yields have pressured the A-share market recently, we expect the impact to lessen going forward. Having said that, we reiterate our view that large index gains aren’t the opportunities we look for. Instead, we see more opportunities coming from styles and sectors in 2Q21. Our analysis shows that during periods of rising US Treasury yields, growth stocks underperform in the short term, but outperform in the long term, as the bullish outlook for growth offsets worries about high valuations. Indeed, we see investors favoring growth stocks given China’s economy and policies are normalizing post the pandemic, while the 14th Five-year Plan provides optimism for high-growth sectors.

2. Will funds rotate from large-caps to mid-caps? We see the earnings growth recovery as the key driver for the outperformance of the mid-cap sector. We think improving profits will reassure investors, so the valuation premium that big caps have benefited from due to their high earnings visibility will shrink. Currently, the consensus earnings growth (2020/2021 CAGR) of mid/small caps is set to beat large caps. As a result, we see investors increasingly turning to mid/small caps. However, we are cautious on small caps given an increasing supply due to the revamped IPO system, which could dent the sector’s valuation. Therefore, we prefer mid-cap stocks.

3. Outperforming sectors? We upgrade Consumer Discretionary to overweight, and downgrade Consumer Staples and Healthcare to neutral. We also highlight our seven preferred sub-sectors: chemicals, machinery equipment, electric apparatuses, electronics, light industrial, autos and transportation.

4. Stock ideas. We see the performance of stocks heavily held by institutional investors as only being driven higher by earnings growth, since their valuations are already quite rich. We also screen for 10 mid-cap stocks with the lowest PEGs and present 12 bottom-up stocks ideas from the IT, high-end manufacturing and consumption sectors.

相关报告

国际投行报告-全球芯片行业:芯片的冲突-台积电、三星和英特尔(英)

4179

类型:行研

上传时间:2022-06

标签:投行报告、芯片、冲突)

语言:英文

金额:5积分

HSBC-中国房地产和物业管理行业2022年展望-2021.11.9-75页

3612

类型:行研

上传时间:2021-11

标签:投行报告、房地产、物业)

语言:英文

金额:5积分

汇丰-中国汽车芯片

3295

类型:行研

上传时间:2022-07

标签:汽车、芯片、投行报告)

语言:英文

金额:5积分

世界经济论坛:2021全球风险报告(英文版)

2546

类型:宏观

上传时间:2021-01

标签:全球风险、2021)

语言:英文

金额:5积分

HSBC-全球投资策略之未来城市:城市化形态的变化-2021.4-54页

2471

类型:策略

上传时间:2021-05

标签:投行报告、未来城市、城市化)

语言:英文

金额:5积分

瑞信-2021年全球财富报告(英)

2423

类型:专题

上传时间:2021-06

标签:全球财富、投行报告)

语言:英文

金额:5积分

WTO-2021年世界贸易统计评论

1957

类型:专题

上传时间:2021-08

标签:WTO、2021、世界贸易)

语言:英文

金额:5积分

瑞信-2022全球投资展望:股票、地区和宏观-2021.11.17-194页

1794

类型:宏观

上传时间:2021-11

标签:投行报告、2022投资展望、宏观经济)

语言:英文

金额:5积分

瑞信-全球财富报告2020-2020.10-56页

1614

类型:专题

上传时间:2020-10

标签:全球财富、投行报告)

语言:英文

金额:5积分

瑞信-全球半导体行业:中国集成电路产业的不均衡崛起-2021.1.20-184页

1591

类型:行研

上传时间:2021-01

标签:半导体、中国集成电路、投行报告)

语言:英文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册