微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

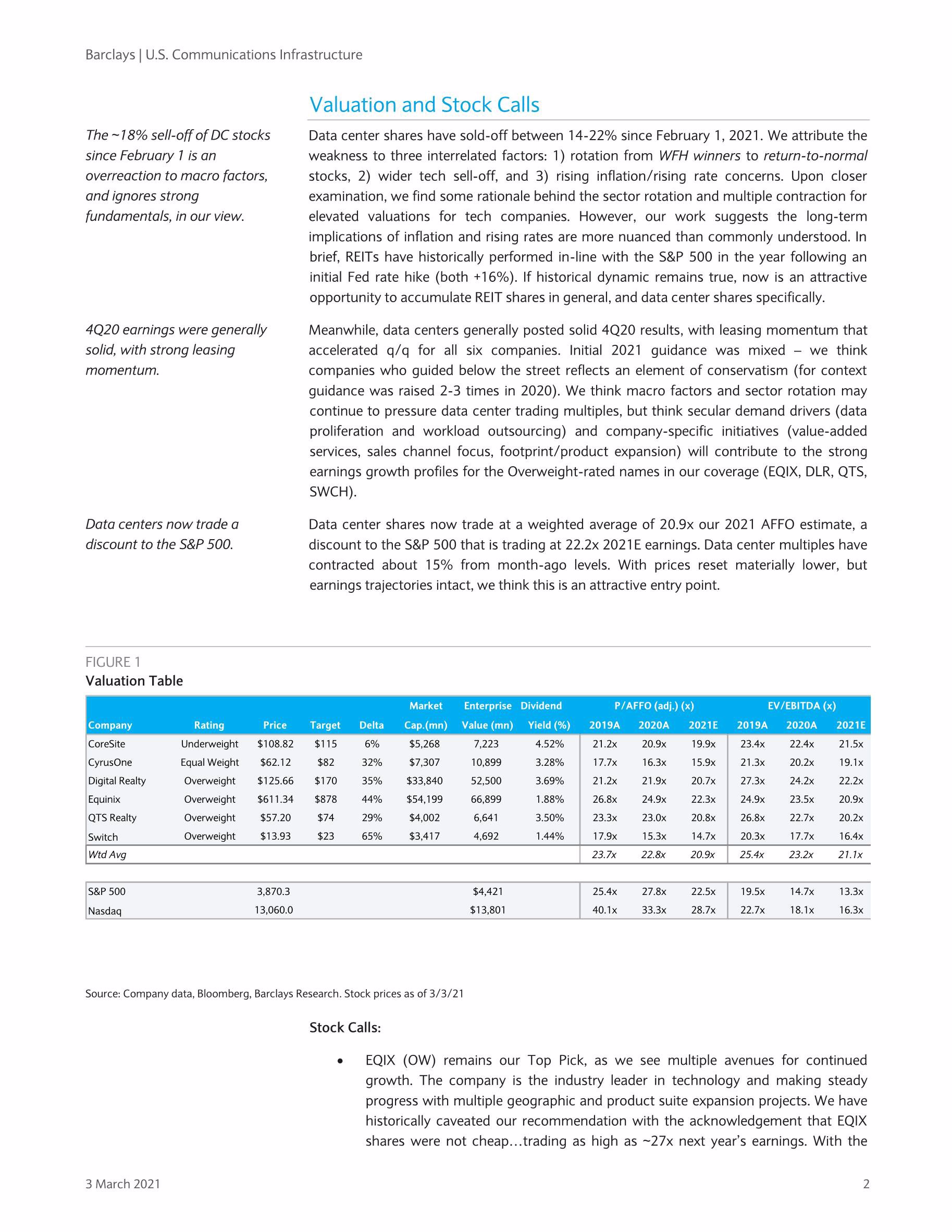

Data center fundamentals a ind underlying secular drivers remain firmly intact. However, data center shares have traded 14-22% lower during the past month, continuing a trend of weakness that started in October 2020. We think this is an attractive point. Our industry view remains positive, and we reiterate our Overweight ratings EQIX DLR QTS, and SWCH Ye attribute share weakness to: 1) rotation from perceived outpefformers amid the pandemic to retur-to-norma/ stocks, 2) broader sell-off of high valuation tech companies, and 3)fears of inflation/rate hiking cycle. We see some rationale for sector rotation and a valuation-reset given emerging growth alternatives as lockdowns abat However, we find the impact of rising rates more nuanced than perceived by the market. Our examination of past hiking cycles indicated both the NAREIT index and S&P 500 appreciated 16% on average in the year following an initial Fed Funds rate hike The sample size is small, but data centers outperformed both indexes in the 2016 cycle Data centers now trade at -21x our 2021 AFFO estimate, compared to -25x a few weeks ago, creating an attractive entry point for exposure to quality earnings streams.

Results from 4020 were generally solid, with leasing momentum accelerating q/q for all six companies. Longer term we think secular dynamics (data proliferation and workload outsourcing )and company specific initiatives(value-added services, sales channel focus, footprint/p expansion)should contribute to% annual earning growth for the foreseeable future We highlight the following opportunities within our coverage universe EQIX(Ow-the industry's technology leader, with an expanding product array and geographic expansion. Shares now trade 22.3x our 2021E AFFO The 1. 5x turn premium to peers is narrow compared to historical trading DLR (OW)-access to attractive capital, skilful land/asset management, expansion in key international markets, and continuous enhancements to its technology offering keep us positive on DLRS growth prospects.

QTS(Ow)-leasing volume increased 44% y/y in 2020, which we attribute to WCH (o)-shares contracted 27% from the 2/10/21(vs S&P-23%)high in response to two 4Q20 churn events. The reaction is overblown, in our view CONE (EW)- Leasing rebounded in 4Q20, instilling confidence in the new management team-but strategic imperatives remain undefined.

COR(UW)-THE company has a compelling technology offering, but eamings growth is below the peer average and churn/backfilling remains an overhang.

相关报告

国际投行报告-全球芯片行业:芯片的冲突-台积电、三星和英特尔(英)

4446

类型:行研

上传时间:2022-06

标签:投行报告、芯片、冲突)

语言:英文

金额:5积分

HSBC-中国房地产和物业管理行业2022年展望-2021.11.9-75页

3788

类型:行研

上传时间:2021-11

标签:投行报告、房地产、物业)

语言:英文

金额:5积分

汇丰-中国汽车芯片

3694

类型:行研

上传时间:2022-07

标签:汽车、芯片、投行报告)

语言:英文

金额:5积分

HSBC-全球投资策略之未来城市:城市化形态的变化-2021.4-54页

2667

类型:策略

上传时间:2021-05

标签:投行报告、未来城市、城市化)

语言:英文

金额:5积分

中国数据中心(中英文版)-46页

2632

类型:专题

上传时间:2021-11

标签:中国、数据中心)

语言:中英

金额:5积分

瑞信-2021年全球财富报告(英)

2543

类型:专题

上传时间:2021-06

标签:全球财富、投行报告)

语言:英文

金额:5积分

国际咨询公司1.3万字报告:2023全球数据中心市场比较(中英对照)

2421

类型:行研

上传时间:2023-12

标签:数据中心、全球市场、发展要素)

语言:中英

金额:3元

瑞信-2022全球投资展望:股票、地区和宏观-2021.11.17-194页

1891

类型:宏观

上传时间:2021-11

标签:投行报告、2022投资展望、宏观经济)

语言:英文

金额:5积分

瑞信-全球半导体行业:中国集成电路产业的不均衡崛起-2021.1.20-184页

1738

类型:行研

上传时间:2021-01

标签:半导体、中国集成电路、投行报告)

语言:英文

金额:5积分

瑞信-全球财富报告2020-2020.10-56页

1701

类型:专题

上传时间:2020-10

标签:全球财富、投行报告)

语言:英文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册