微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

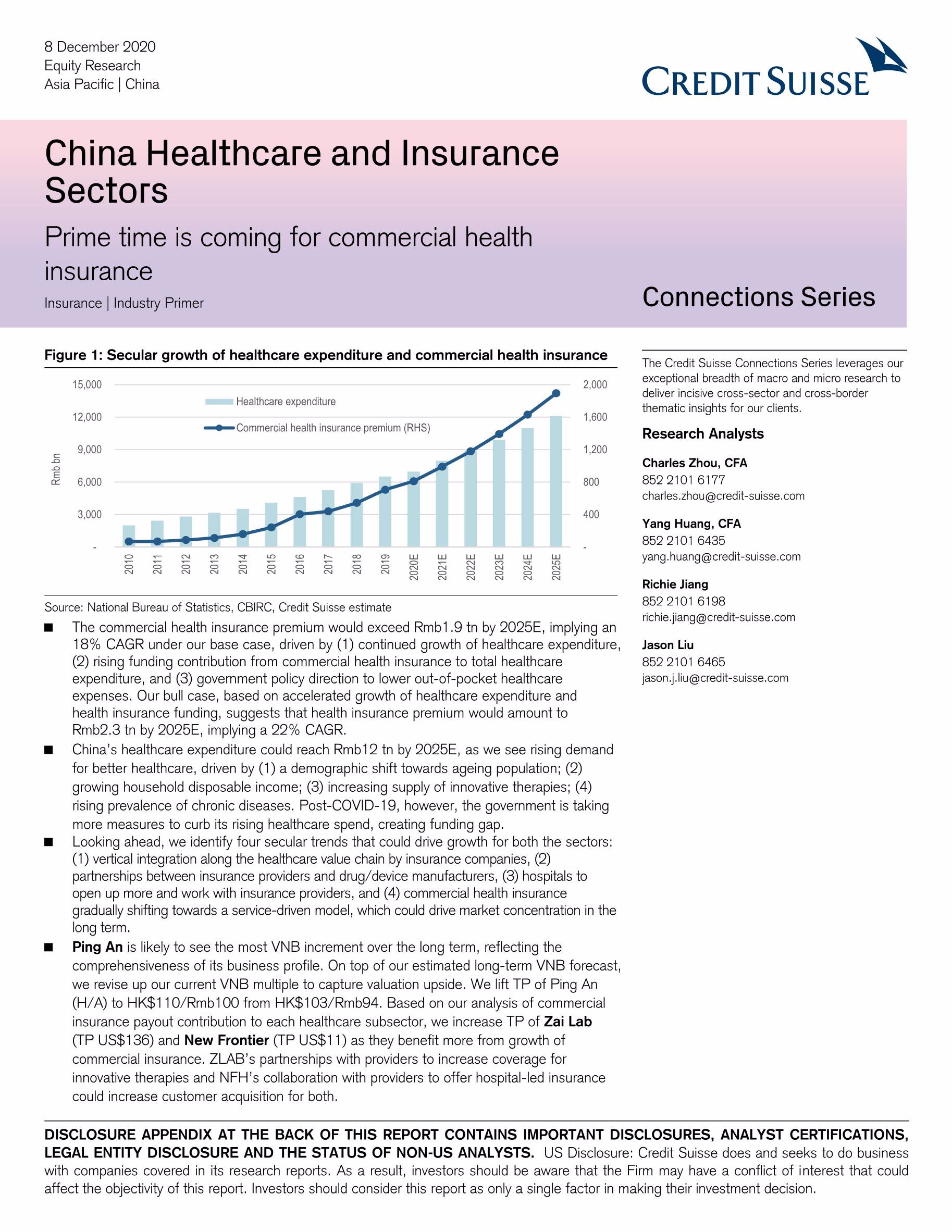

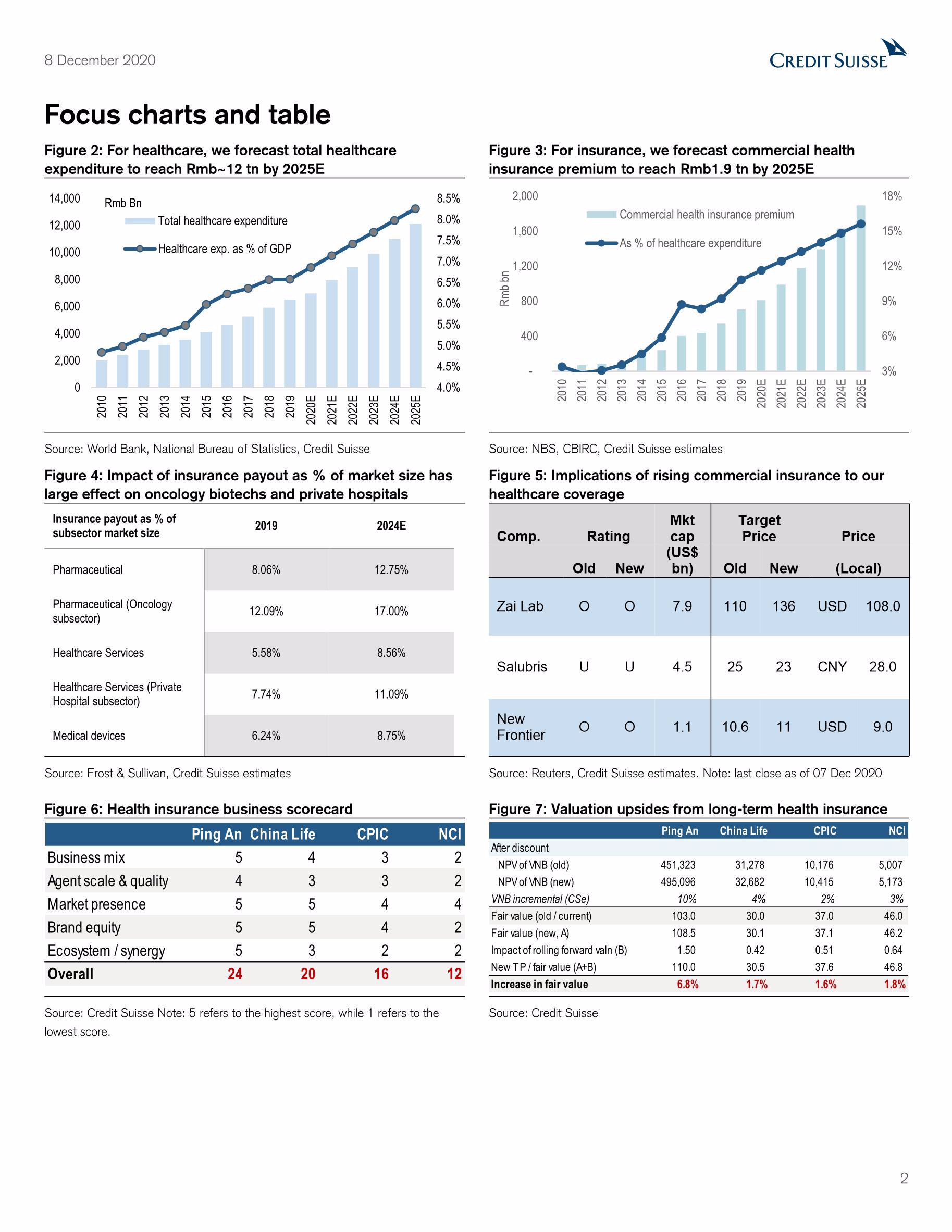

The commercial health insurance premium would exceed Rmb1.9 tn by 2025E, implying an 18% CAGR under our base case, driven by (1) continued growth of healthcare expenditure, (2) rising funding contribution from commercial health insurance to total healthcare expenditure, and (3) government policy direction to lower out-of-pocket healthcare expenses. Our bull case, based on accelerated growth of healthcare expenditure and health insurance funding, suggests that health insurance premium would amount to Rmb2.3 tn by 2025E, implying a 22% CAGR.

China’s healthcare expenditure could reach Rmb12 tn by 2025E, as we see rising demand for better healthcare, driven by (1) a demographic shift towards ageing population; (2) growing household disposable income; (3) increasing supply of innovative therapies; (4) rising prevalence of chronic diseases. Post-COVID-19, however, the government is taking more measures to curb its rising healthcare spend, creating funding gap.

Looking ahead, we identify four secular trends that could drive growth for both the sectors: (1) vertical integration along the healthcare value chain by insurance companies, (2) partnerships between insurance providers and drug/device manufacturers, (3) hospitals to open up more and work with insurance providers, and (4) commercial health insurance gradually shifting towards a service-driven model, which could drive market concentration in the long term.

Ping An is likely to see the most VNB increment over the long term, reflecting the comprehensiveness of its business profile. On top of our estimated long-term VNB forecast, we revise up our current VNB multiple to capture valuation upside. We lift TP of Ping An (H/A) to HK$110/Rmb100 from HK$103/Rmb94. Based on our analysis of commercial insurance payout contribution to each healthcare subsector, we increase TP of Zai Lab (TP US$136) and New Frontier (TP US$11) as they benefit more from growth of commercial insurance. ZLAB’s partnerships with providers to increase coverage for innovative therapies and NFH’s collaboration with providers to offer hospital-led insurance could increase customer acquisition for both.

相关报告

《攒多少钱才能安心养老》-写给中国人的养老指南-读书笔记

5067

类型:读书笔记

上传时间:2023-04

标签:社保、退休养老、保险)

语言:中文

金额:9.9元

《做自己的保险规划师》读书笔记 :明白买保险,安心过一生

2887

类型:读书笔记

上传时间:2023-03

标签:保险、养老、财富规划)

语言:中文

金额:9.9元

懂法律,大保单销售不再难,给成交一个法律的理由——《懂法律,成交更简单》—读书笔记

2243

类型:读书笔记

上传时间:2024-07

标签:营销、保险、销售)

语言:中文

金额:9.9元

2025大中华高净值人士财富传承与保险规划报告

2149

类型:行研

上传时间:2025-02

标签:高净值人士、财富、保险)

语言:中文

金额:5积分

图解国家金融监督管理总局《银行保险机构数据安全管理办法》(征)V1.0.0

1564

类型:政策法规

上传时间:2024-04

标签:银行、保险、数据安全)

语言:中文

金额:5积分

全球保险业报告:展望亚洲财险业的未来

1425

类型:行研

上传时间:2024-11

标签:保险)

语言:中文

金额:5积分

2024中国保险代理人岗位研究报告

1285

类型:行研

上传时间:2024-02

标签:保险、代理人、岗位)

语言:中文

金额:5积分

重疾险销售资料

1279

类型:投资理财

上传时间:2025-06

标签:重疾险、保险、健康)

语言:中文

金额:15积分

2024年中国互联网保险消费者洞察报告

1052

类型:行研

上传时间:2025-06

标签:保险、消费者)

语言:中文

金额:5积分

2024带病体保险创新研究报告

1026

类型:行研

上传时间:2024-02

标签:带病体、保险、健康险)

语言:中文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册