微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

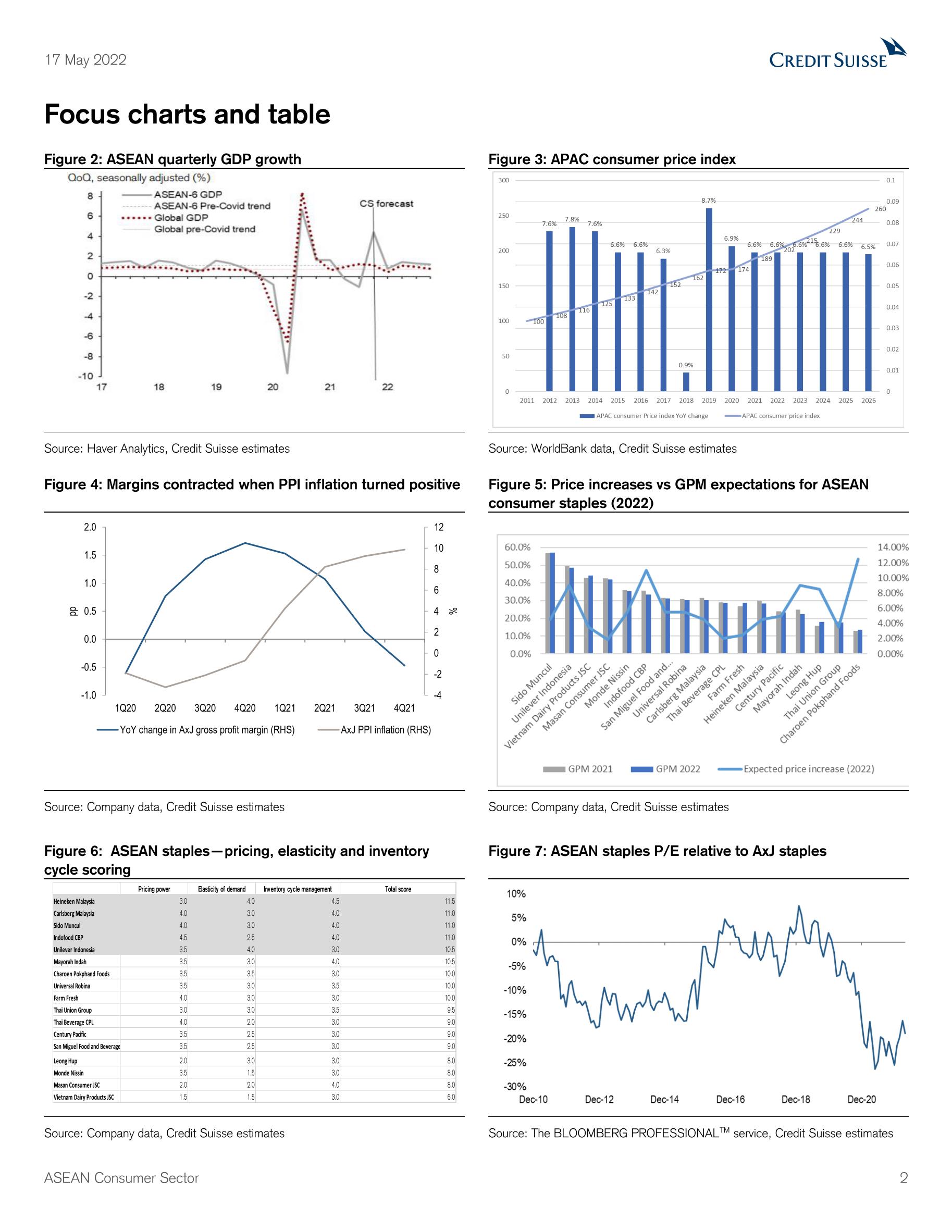

High inflation and rising commodity prices (oil, wheat, and packaging) are negatives, both through inflation and higher costs, as oil and soft commodity prices continue to rise. In terms of impact on countries, energy and commodity exporters (Indonesia and Malaysia), should remain resilient, but at the losing end would be the Philippines (heavy reliance on imported oil), Vietnam and Thailand; these may face the brunt of the commodity price spike. Here we assess further the potential impact of higher commodity prices on the ASEAN consumer space, especially the manufacturers that are likely to be hardest hit. Our overall analysis shows that EPS risk is higher for food manufacturers, as other sub-sectors, such as retailers and home improvement counters, commodity/suppliers and food service, will likely be more defensive (but not immune) against cost shocks. The extent of additional inflationary pressure, however, will fundamentally depend on three things: (1) pricing strategy, (2) inventory management, (3) elasticity of consumers to rising prices. Gross margin expectations for staples show that companies high in our score card are likely to have resilient margins in the next two years. Companies that scored high in our ranking were Heineken, Carlsberg, Unilever Indonesia, Sido & Indofood, while lower score companies were Century Pacific, San Miguel F&B, Masan, Vietnam Dairy & Monde Nissin. While most stocks in our ASEAN consumer coverage are trading below their pre-Covid 19 levels (using 31-Dec-2019 as a proxy), we are cognizant of the risks. During past oil shocks, the performance of staples and discretionary segments in ASEAN seem to move in the same direction, but a more pronounced derating can be seen for discretionary stocks. Historical evidence shows that staples tend to bounce back faster than discretionary post peak, and that both segments have a negative correlation to rising prices of oil. We prefer our fundamental framework of names that are top franchises in ASEAN, with bias towards retailers and select food service companies: CPALL, SIDO, FARM, PNJ, and JFC.

相关报告

1.3万字报告:2024年美国经济展望(中英对照)

4727

类型:宏观

上传时间:2023-11

标签:美国经济、通货膨胀、地缘政治)

语言:中英

金额:5元

联合国9万字报告:2023年世界经济形势与展望(中英文版)

4491

类型:宏观

上传时间:2023-02

标签:联合国、经济展望、通货膨胀)

语言:中英

金额:15元

国际投行报告-全球芯片行业:芯片的冲突-台积电、三星和英特尔(英)

4446

类型:行研

上传时间:2022-06

标签:投行报告、芯片、冲突)

语言:英文

金额:5积分

HSBC-中国房地产和物业管理行业2022年展望-2021.11.9-75页

3788

类型:行研

上传时间:2021-11

标签:投行报告、房地产、物业)

语言:英文

金额:5积分

汇丰-中国汽车芯片

3694

类型:行研

上传时间:2022-07

标签:汽车、芯片、投行报告)

语言:英文

金额:5积分

宏观经济通识课-70页-读书笔记

3178

类型:读书笔记

上传时间:2022-08

标签:宏观经济、读书笔记、通货膨胀)

语言:中文

金额:6.6元

HSBC-全球投资策略之未来城市:城市化形态的变化-2021.4-54页

2667

类型:策略

上传时间:2021-05

标签:投行报告、未来城市、城市化)

语言:英文

金额:5积分

瑞信-2021年全球财富报告(英)

2543

类型:专题

上传时间:2021-06

标签:全球财富、投行报告)

语言:英文

金额:5积分

最新翻译美联储4.7万字报告:2022年上半年货币政策总结(中英对照)

1916

类型:宏观

上传时间:2022-07

标签:劳动力、通货膨胀、全球经济)

语言:中英

金额:7元

瑞信-2022全球投资展望:股票、地区和宏观-2021.11.17-194页

1891

类型:宏观

上传时间:2021-11

标签:投行报告、2022投资展望、宏观经济)

语言:英文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册