微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

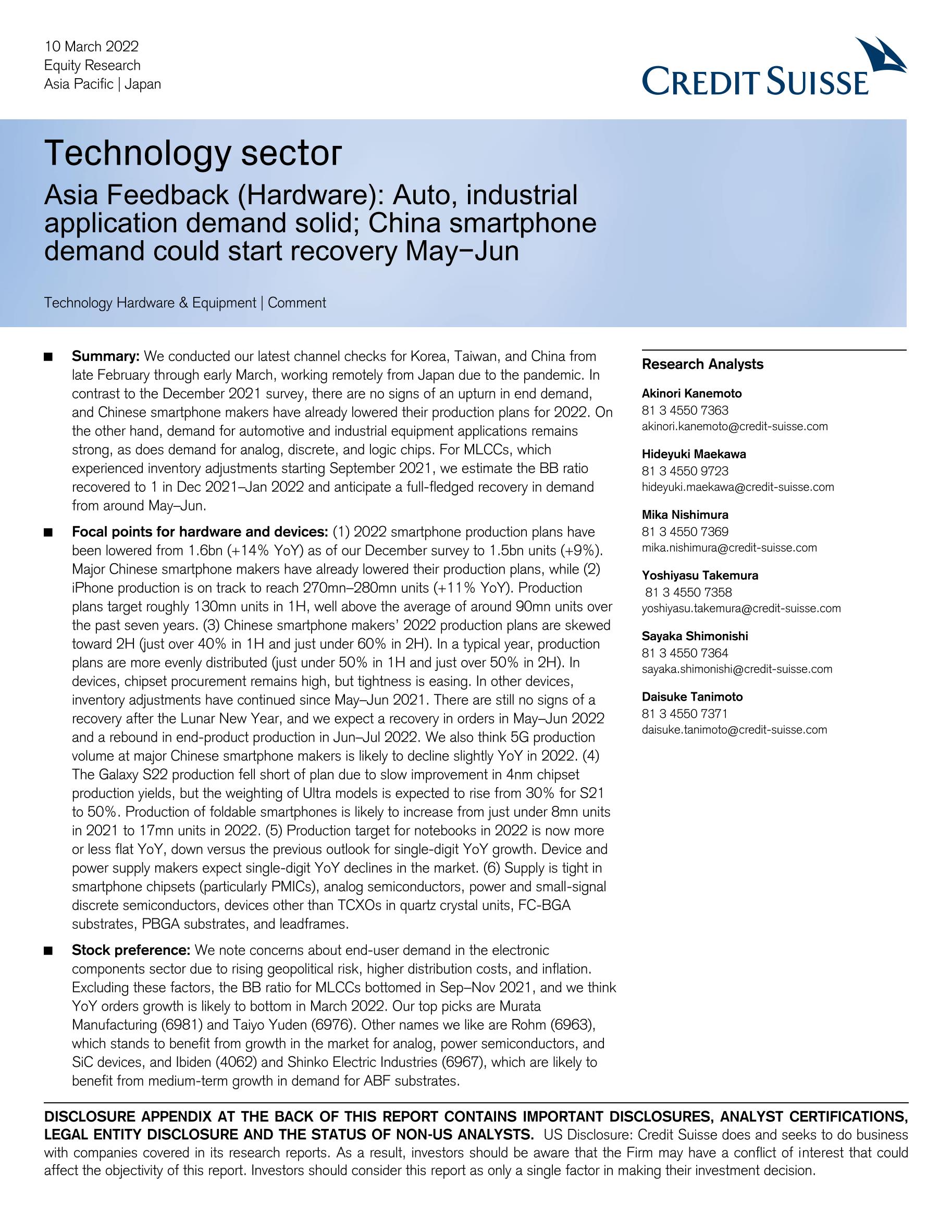

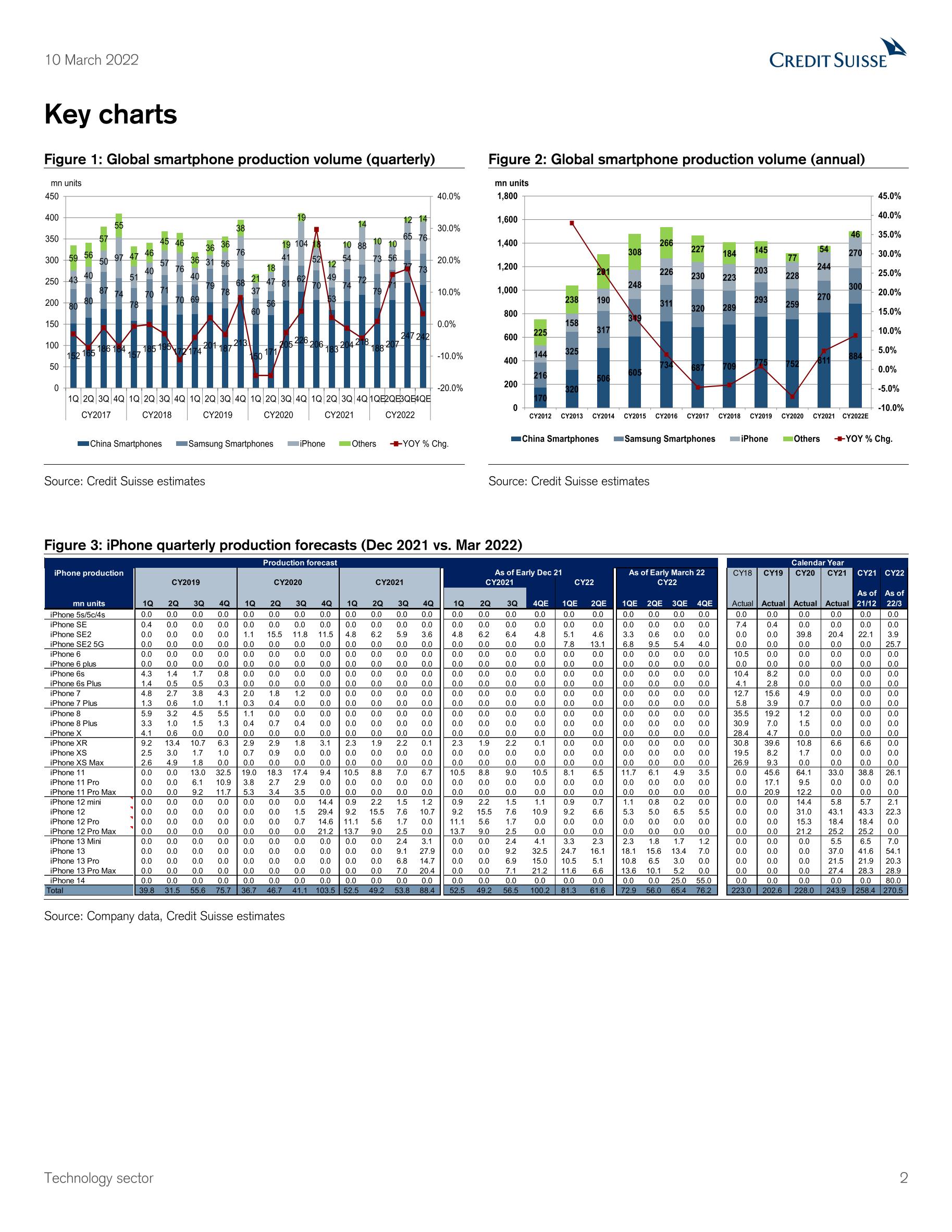

Summary: We conducted our latest channel checks for Korea, Taiwan, and China from late February through early March, working remotely from Japan due to the pandemic. In contrast to the December 2021 survey, there are no signs of an upturn in end demand, and Chinese smartphone makers have already lowered their production plans for 2022. On the other hand, demand for automotive and industrial equipment applications remains strong, as does demand for analog, discrete, and logic chips. For MLCCs, which experienced inventory adjustments starting September 2021, we estimate the BB ratio recovered to 1 in Dec 2021–Jan 2022 and anticipate a full-fledged recovery in demand from around May–Jun. Focal points for hardware and devices: (1) 2022 smartphone production plans have been lowered from 1.6bn (+14% YoY) as of our December survey to 1.5bn units (+9%). Major Chinese smartphone makers have already lowered their production plans, while (2) iPhone production is on track to reach 270mn–280mn units (+11% YoY). Production plans target roughly 130mn units in 1H, well above the average of around 90mn units over the past seven years. (3) Chinese smartphone makers’ 2022 production plans are skewed toward 2H (just over 40% in 1H and just under 60% in 2H). In a typical year, production plans are more evenly distributed (just under 50% in 1H and just over 50% in 2H). In devices, chipset procurement remains high, but tightness is easing. In other devices, inventory adjustments have continued since May–Jun 2021. There are still no signs of a recovery after the Lunar New Year, and we expect a recovery in orders in May–Jun 2022 and a rebound in end-product production in Jun–Jul 2022. We also think 5G production volume at major Chinese smartphone makers is likely to decline slightly YoY in 2022. (4) The Galaxy S22 production fell short of plan due to slow improvement in 4nm chipset production yields, but the weighting of Ultra models is expected to rise from 30% for S21 to 50%. Production of foldable smartphones is likely to increase from just under 8mn units in 2021 to 17mn units in 2022. (5) Production target for notebooks in 2022 is now more or less flat YoY, down versus the previous outlook for single-digit YoY growth. Device and power supply makers expect single-digit YoY declines in the market. (6) Supply is tight in smartphone chipsets (particularly PMICs), analog semiconductors, power and small-signal discrete semiconductors, devices other than TCXOs in quartz crystal units, FC-BGA substrates, PBGA substrates, and leadframes. Stock preference: We note concerns about end-user demand in the electronic components sector due to rising geopolitical risk, higher distribution costs, and inflation. Excluding these factors, the BB ratio for MLCCs bottomed in Sep–Nov 2021, and we think YoY orders growth is likely to bottom in March 2022. Our top picks are Murata Manufacturing (6981) and Taiyo Yuden (6976). Other names we like are Rohm (6963), which stands to benefit from growth in the market for analog, power semiconductors, and SiC devices, and Ibiden (4062) and Shinko Electric Industries (6967), which are likely to benefit from medium-term growth in demand for ABF substrates.

相关报告

《汽车企业数字化转型:认知与实现》读书笔记

7233

类型:读书笔记

上传时间:2022-01

标签:数字化转型、汽车、大数据)

语言:中文

金额:9.9元

国际投行报告-全球芯片行业:芯片的冲突-台积电、三星和英特尔(英)

4446

类型:行研

上传时间:2022-06

标签:投行报告、芯片、冲突)

语言:英文

金额:5积分

HSBC-中国房地产和物业管理行业2022年展望-2021.11.9-75页

3788

类型:行研

上传时间:2021-11

标签:投行报告、房地产、物业)

语言:英文

金额:5积分

汇丰-中国汽车芯片

3694

类型:行研

上传时间:2022-07

标签:汽车、芯片、投行报告)

语言:英文

金额:5积分

预见2025-中国行业趋势报告:2025六大热门话题、八大行业趋势:汽车、材料、消费、科技、健康

3508

类型:行研

上传时间:2025-02

标签:汽车、材料、消费)

语言:中文

金额:5积分

2024中国汽车消费者洞察报告

2683

类型:行研

上传时间:2024-03

标签:汽车、消费者)

语言:中文

金额:5积分

HSBC-全球投资策略之未来城市:城市化形态的变化-2021.4-54页

2667

类型:策略

上传时间:2021-05

标签:投行报告、未来城市、城市化)

语言:英文

金额:5积分

瑞信-2021年全球财富报告(英)

2543

类型:专题

上传时间:2021-06

标签:全球财富、投行报告)

语言:英文

金额:5积分

2024中企全球化销售人才报告:汽车行业出海与全球化

2430

类型:行研

上传时间:2024-05

标签:销售人才、出海、汽车)

语言:中文

金额:5积分

汽车行业智能驾驶-Robotaxi:产业化大幕开启,无人驾驶未来已来-240716-47页

2268

类型:行研

上传时间:2024-07

标签:汽车、智能驾驶)

语言:中文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册